|

THURSDAY EDITION July 23rd, 2026 |

|

Home :: Archives :: Contact |

|

|

Scrap in the Time of ScarcityRichard KarnEmerging Trends Report January 14, 2008 Executive Summary: At first glance, this quarter's Emerging Trends Report (ETR) on base metal recycling and specialty metal toll refining, with a secondary emphasis on tailings reprocessing and catalysis, may appear to be something of a departure. The ETR, however, views these sectors as being entirely consistent with our approach of investing only in the safest, most basic aspects of an economy as all three will benefit directly from both a number of our infrastructure themes as well as the far higher energy and commodity prices we see being loaded into the market pipeline today. The short version of our thinking goes like this. In response to the deflationary pressures exerted by the Credit Crisis, central banks globally are expanding money supply at unprecedented rates, which assuming their efforts are successful can only result in higher energy and commodity prices-where the rubber (fiat currency purchasing power) meets the road (hard assets). As has consistently been the case for the last twenty years, however, reflation efforts will also produce a host of unintended consequences, a few of which from the last effort are even today serving to impede the progress of a number of energy and commodity mega-projects widely expected to ease existing supply constraints. Going forward, the ETR anticipates the unintended consequences from this reflation effort to include:

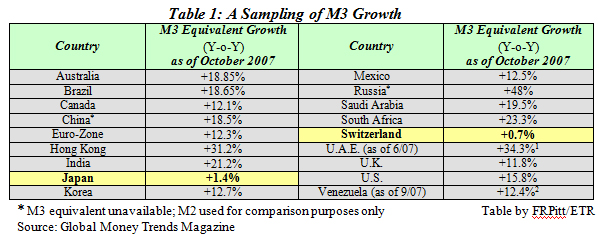

In an investment climate such as the one outlined above, companies that can help increase the supply of commodities, reduce energy consumption, ensure the supply of critical metals, and improve process efficiencies stand to profit disproportionately. This quarter's Emerging Trends Report focuses on exactly these companies, blending the unglamorous with the exotic, the practical with the fantastic; it explores the profit potential of doing more with less. We have put together a portfolio of 18 recommendations, ranging from century-old firms to recent start-ups, ideally positioned to profit from the coming emphasis on economy in a world of high inflation and scarcity, and as is our practice none bear significant sovereign risk. EDITOR'S NOTE: For subscribers looking for a discussion of monetary inflation and what it means to their economic well-being, we have taken the liberty of attaching an appendix at the end of this report. For general readers interested in a rudimentary discussion of fiat currencies and monetary inflation, we invite them to download "The Gold Treatment" available free of charge at http://www.emergingtrendsreport.com. Detail 1: Double Whoopee In regard to the current Credit Crisis, the image that comes to mind is of Laurel and Hardy furiously bucketing water from a wall spigot into a large belching contraption that they fail to realize has a valve at its base wide open, so their efforts are slowly flooding the room. Sweating profusely as the machine overheats and the water rises around them, Bernanke's Hardy turns to Greenspan's Laurel and says, "Well, here's another nice mess you've gotten me into." As we go to press in January of 2008, global financial markets are profoundly conflicted. On the one hand markets are holding their collective breaths not over what the US central bank response will be to the latest crisis, for that is a forgone conclusion, but over whether it can work one more time. The fear is that twenty years of uniform policy response, that being to suppress interest rates and to pump liquidity into the financial system, will have finally caught up with central bankers and they may not be able to replace the liquidity gushing out of the system as a result of the malfeasance of financial institutions fast enough to keep the system from running dry and seizing up. At the same time, markets are also giddy with anticipation. The thought of all of that liquidity, as measured by M3 equivalent, being pumped into the global financial system, which if the reflation efforts succeed will have to go somewhere, makes them salivate:

The Crash of '87, the S&L Crisis, the Asian Crisis, LTCM, Y2K, the Tech Bubble, the Housing Bubble which turns out to be a far larger and more debilitating Credit Crisis: about every three years the liquidity pumped into the system in response to the last financial crisis creates a new and larger one, prompting another round of stimulus, each larger than the last but producing less actual growth in Gross Domestic Product (GDP) for the expansion of the monetary base needed to produce it. But, man, is there money to be made between crises, and the markets can see from the preceding table that speculation is still the order of the day. Whereas central banks worldwide are pumping liquidity into the system at unprecedented rates to stop the hemorrhaging, the Japanese and Swiss are not: the glaring stability in these two currencies, which is crucial for the implementation of the spectacularly leveraged carry trade, means it is still game on. But the trillion dollar question is: where is all of that new money headed? Ironically, even if central bankers are successful in their reflation efforts, they may not like the next bubble likely to inflate because the odds are very good it will be in commodities. Over time the effects of previous bouts of monetary expansion, especially if the excess liquidity is not gradually drained from the system to rebalance it after a crisis has passed, have the cumulative effect of accelerating a currency's loss of purchasing power, most tellingly in terms of real goods and services. History has demonstrated time and again that monetary policy affects energy and commodity prices disproportionately, and this reflation effort is being initiated at a time when monetary policy is already remarkably inflationary. In this regard, the ETR has been chronicling anomalous corollary market behavior clearly indicating that an acceleration in the general decline of all fiat currencies is well underway, regardless of how they are performing against each other. Common folks, not just sovereign funds, are recognizing the negative real interest rate environment fostered by the Federal Reserve Bank's ludicrous Consumer Price Index (CPI) claims, which are being used as justification to lower interest rates further in response to the latest crisis, and as interest rates decline so do the opportunity costs of holding commodities, making them more attractive. What has developed globally over the last decade has been a legitimate boom in energy and commodities resulting from a very real and growing supply-demand imbalance. True, it has been exaggerated by speculation and various risk premiums, but unlike financial instruments energy and commodities are in short supply and cannot simply be conjured by fingers dancing on the keys of a computer. And that is the makings of the next calamity, for where a commodity boom in itself is a relatively low level threat to the central banking system, the very speculation central banking policies actively promote over time can also engender a commodity bubble, which is a central banker's worst nightmare. Under a fiat currency regime, monetary inflation, when properly managed, exercises a controlled erosion of the currency's value, incrementally chipping away at a population's savings and ever so slowly but relentlessly increasing the prices of things that cannot also be conjured. The ETR has argued in the past that perhaps the reason central banks target a 2-3% annual inflation rate is because that is the level a population seems to tolerate without complaint. Be that as it may, financial booms generally reflect prosperity and develop into bubbles as a result of the greed unleashed by overly accommodative monetary policy as those in financial circles, who are not coincidentally closest to the creation of the new money and credit, reap immeasurable profits. Conversely, commodity booms are born in response to supply-demand imbalances but grow into bubbles out of fear-the fear that results when a populace realizes the nominal gains it took for the trappings of wealth were but a financial slight of hand that have actually amounted to losses in real purchasing power. This recognition means central bankers have lost control of the nominal value of their currencies, prompting wholesale changes in the price discovery mechanism, and the subsequent surprise at how little the currency can actually buy develops first into a desire to hoard and then into a full-fledged panic to acquire tangible assets of intrinsic value before the currency depreciates further into what is known as hyperinflation, the death knell of 20 fiat currencies in the 20th century alone. The ETR is not suggesting the US dollar is entering hyperinflation and is on the verge of collapse at this time because the reflation efforts are being supported and coordinated on a global basis. However, the unprecedented level of monetary expansion will amount to another step in that direction as the purchasing power of the dollar will surely decline at a faster rate as a result of these actions. What we believe is the critical consideration at this juncture is that this reflation effort exposes and exacerbates the primary weakness of a fiat currency regime: the market simply cannot efficiently price real goods and services in terms of the rapidly fluctuating nominal value of a fiat currency because it is always behind the curve-- always reacting to, not anticipating, the effects of monetary inflation. As awareness of this lopsided relationship becomes widespread, the market will tend to err on the side of higher prices in the future. What the table on page 2 suggests then is that the unprecedented monetary inflation being unleashed in response to the Credit Crisis today will further destabilize world energy and commodity markets tomorrow: the ETR can but conclude that markedly higher prices and increased volatility are imminent and will become a permanent aspect of global markets. Detail 2: "There must be some kind of way out of here Said the joker to the thief There's too much confusion I can't get no relief" To garner an idea of what is heading our way, consider the effects the unintended consequences from the last bout of monetary inflation are having as they work their way through the system today. Occasionally, something pops up that brings this loss of purchasing power into an uncomfortable focus, such as what transpired in early November 2007 at the World Energy Congress in Rome. When Rex Tillerson, the CEO of Exxon Mobil, was being queried about the market's ability to respond to $98 per barrel oil, he replied that in addition to the tightness in supply, there were other factors involved, citing as an example oil price subsidies in some countries that meant demand destruction didn't occur as it would in the US or Europe. According to NYMEX: "Tillerson noted that the weak dollar is another key factor in the rising price of oil, adding that crude would be $20 to $25 per barrel cheaper if the dollar had remained stable." Certainly, various catastrophe premiums are built into the prices of all commodities, whether related to terrorism or impending conflict, resource nationalism, Peak Oil or Peak Soil, weather, or reduced stockpiles of material, but this was a rare public comment directly implicating the contribution of dollar devaluation to the current energy pricing structure. Whether this level of monetary inflation is consistent in all commodity prices is debatable; what is not, however, is that the price of oil contributes significantly to the cost structure of virtually all other commodities. Interestingly, Tillerson's comment was met with a resounding silence on the part of the US media, but the ETR suspects the matter is rapidly becoming simply too large to ignore. These unintended consequences of monetary inflation are also showing up today as an epidemic of cost increases and over-runs in the very projects widely expected to ease various supply bottlenecks in the years ahead, which can only mean those higher costs are going to be passed on to consumers. Consider but a few recent examples (emphasis added):

Against this backdrop, the immediate availability, abundance and energy savings inherent to the base metal recycling industry makes it a vital as well as reliable source of new material-especially in developed countries. This is due in large part to a metal's very nature rendering it infinitely re-useable, for as a metal is recycled, melting the metal returns it to its basic elemental structure, meaning there is negligible difference between primary (freshly mined ore) and secondary (scrap) sources of material feedstock, other than the vast energy savings found in using scrap as the feedstock. This differs from other commonly recycled materials such as paper, which because it is cellular-based the actual fibers deteriorate with each recycling, producing a lower quality product each time and eventually leading to it being composted. The market also tends to overlook the notion that the more developed the economy, the more scrap it generates and has available to both to meet its needs and for export, as is witnessed for example by scrap metal being the US' second largest export to China in 2006. In this regard, the US may be the first country in history to reach the milestone known as resource equilibrium in iron (please refer to Detail 3 below). Cambridge Energy Research Associates (CERA) also sees this trend of cost over runs contributing to the constriction of oil and gas supply going forward. For example, of the projects under development promising a 4% annual increase in global oil refining capacity over the next 5 years, CERA now believes only about 1.7% each year will actually get built due to the combination of escalating costs and the increased lead times needed to secure sophisticated equipment, which has doubled in the last 6-12 months. Although there is no substitute for additional capacity, improved process efficiencies, especially as it applies to catalysis in the refining and petrochemical industries, holds remarkable promise for making better use of what will be available in the years ahead. Ironically, however, despite the Credit Crisis, or perhaps because of it, banks that are terrified of lending to each other for fear of holding each others' paper do not experience similar qualms about extending mining project financing-albeit selectively. This speaks volumes regarding the investment banking community's opinion of the performance of the notional in relation to the real. Considering the rate of monetary inflation and extent of cost over runs, however, banks could end up being well-positioned to become far larger partners in such projects than originally envisioned. None of this is lost on commodity-producing nations, of course, who are understandably bitter about trading their finite natural resources for fiat currency, the value of which is dissolving like a sugar cube in the rain. Calls by the US and others to increase production to alleviate the cost of the real in terms of the fiat will fall on increasingly deaf ears as doing so is becoming increasingly inimical to the interests of producer nations. Where previously commodity-producing nations have had little choice but to price their natural resources in US dollars, a groundswell is gaining momentum to price production in anything but dollars. However, this will accomplish little because the whole world is practicing what is oxymoronically termed 'competitive currency devaluation'-- as if there were some kind of prize to be won by the country that can bankrupt its citizens first. A mere glance at the charts of agricultural products, oil or gold in any fiat currency reveals a pattern reminiscent of that of the dollar, rendering the efficacy of such a move moot. Frustrated or opportunistic, many countries feel they have been victims of a conspiracy to defraud and feel justified in exacting retribution on whatever is handy since they have been unable to engage the United States directly for redress. Egged on by populist leaders, the appeal and political mileage to be made from this behavior should not be underestimated. Unfortunately, what is handy are US and OECD energy and commodity operations that are increasingly becoming subject to a growing spate of 'adjustments' to the way they are allowed to conduct business-that is, if they are allowed to continue at all. Donald Coxe summed it up thus: political risk increases at the square of the commodity price increase. But where Mr. Coxe was addressing his formula to Third World countries, what has in fact occurred in response to energy and commodity prices at or near record nominal prices is that governments everywhere, even in the US and Canada, are violating contracts in order to cut themselves in on the action in the form of increased royalties, taxes or outright theft in the form of nationalization. A partial list of 'policy changes' just since the release of our transportation fuels report in July is sobering:

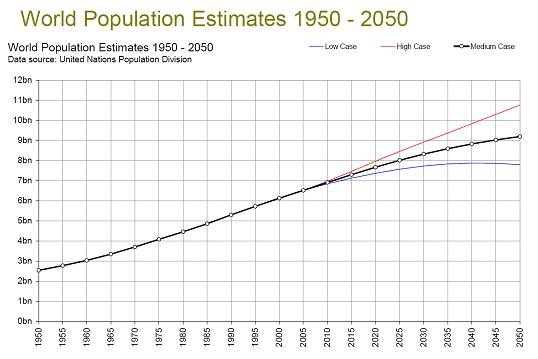

According to Control Risk, a British consultancy which rates 57% of emerging markets at medium or higher political risk: "Political risk is back and should be worrying investors." It is certainly worrying mining executives today, many of whom are understandably loath to undertake company-breaking investment risks in a country that may simply allow them to develop a project, put it into production and then nationalize the operation out from under them. In this regard, the US and OECD are especially vulnerable as the majority of what are known as "critical metals" employed in myriad technology and defense applications have foreign origins. With the US Strategic Stockpile sold off or never having contained these metals to start with, recent hoarding of such metals by South Korea, Japan and China, and the environmental nightmares involved with permitting new mines in the US, specialty metal toll refiners have emerged as secure, significant, and reliable sources of such materials (please refer to Detail 4 below). Of all of the risks to future resource development, the ETR views those attendant to political agendas as being the most significant, for without direct foreign investment, engineering and technical expertise, many of the large energy and mining projects the world needs cannot be undertaken. That is, unless you are more concerned with strategic than commercial objectives. Sustained high energy and commodity prices have put national resource companies and their sovereign fund counterparts in the position to step in to fill the void should OECD companies abandon or be ousted from development projects. However, because their motivations are the strategic acquisition and control of resources to support their economies and political agendas rather than mere profit, what comes on line from such sources either may not reach the open markets at all or come attached with myriad unpalatable conditions. Commodity-producing nations, many of whom have been feeling short-changed by their dealings with the west, now have another set of buyers in the surplus-generating Asian nations who are willing to pay higher prices in order to keep their growing economies supplied. This marks a significant departure from the metrics under which the markets have operated for at least 3 decades: one that presents a serious threat to the status quo in that it is not a matter of other economies decoupling from the US during a downturn but an entire shift in approach to long term resource acquisition. And these organizations have more than enough money to finance any project. Sovereign wealth funds now control more than $2.2 trillion of assets and foreign currency reserves and have been experiencing mid-tier growth of 19.8% for the last five years. Fourteen of the twenty largest sovereign funds represent commodity-based economies, and by 2012 the International Monetary Fund (IMF) estimates aggregate foreign assets under sovereign management will reach $12 trillion-- at least four times what is under management today by hedge and private equity funds combined. For China and India in particular, guaranteeing long term supplies of energy and commodities for their economies far outweigh price concerns. Across Africa and South America in particular, but Central Asia as well, they are forging long term relationships with resource-rich, infrastructure-poor countries that are generous, based solely on commerce and come without high-minded conditions. Being presented an alternative to the paternalistic IMF-World Bank model, the ETR expects many more countries, especially in Africa, to establish warm ties with China and India. This is already reviving a de facto most-favored nation bias that can only lead to multiple pricing structures destined to have a negative effect on the functioning of free markets. It is also becoming apparent that nations are increasingly reluctant to hold each other's debt. As it stands, sovereign funds and national resource companies, notably those of Russia, China and the Middle East, are determined to spend their US dollars before their value is diminished further and are using every opportunity to purchase producing assets, reserves and technology all over the world. This newfound political and economic power also raises issues ranging from the observance of intellectual property rights to a broad re-thinking of what constitutes a strategic asset. Since national resource companies and sovereign funds are not subject to oversight, and few are as unobtrusive and transparent as that of Norway, politicians throughout the developed world are stoking protectionist fires, which regardless of how valid the concerns may be is rarely constructive, especially considering a few of the West's vulnerabilities regarding supply. What is developing is a volatile situation wherein OECD countries and the rest of the world are playing by differing sets of rules, pitting free market proponents against national mercantilists, and an unpleasant collision is on the horizon. This, the ETR believes, in turn will prompt a new wave of mergers and acquisitions, typified by that underway in the mining industry. As a survival mechanism, if a company can become large enough, not only does its sheer size make it less likely to be a take-over target but also it can attain a kind of protectionist immunity by becoming of strategic importance to its home country. The ETR predicts this will be the case in the widely publicized takeover of Rio Tinto by BHP Billiton: in the end, even if it means paying more than anticipated, BHP will not pass up the opportunity to use protectionist concerns to trump anti-trust issues; further, as a sap to said anti-trust issues, the merged company will divest itself of assets in those countries it perceives to hold significant sovereign risk. This type of defensive divestiture, as has been exemplified by Encana, is set to increase in lock step with the rate of political interference globally. Another consideration is that energy and commodity companies today have every motivation to purchase existing production, personnel, equipment and reserves rather than attempting to run the finance, environmental permitting, and cost over-run gamut to develop new projects. Though shareholders may be reassured by such growth, in the long run this actually constricts supply in that it merely reshuffles existing resources and assets rather than adding to the general pool of new supply being brought to market, often in the process misallocating funds that previously had been budgeted for exploration and development. Against this backdrop of potential supply constraints, a number of factors indicate global demand is not likely to dissipate significantly for decades to come-if then. Chief among these is the drive by the so-called BRIC (Brazil, Russia, India and China) nations to industrialize, which is a lengthy process requiring significantly higher per capita consumption of base metals and energy throughout the construction stage; once developed, per capita demand tends to find a plateau and energy intensity to relent somewhat albeit at far higher levels of consumption. Because so many of these countries exercise price controls on transportation fuels and electricity to keep their economies booming, demand destruction is not occurring as predicted or as has been the experience in the OECD. Another driver is simply success: as incomes grow, previously unattainable consumer goods are suddenly within reach of rapidly expanding middle classes worldwide. Concurrently, the US, and to a lesser extent Europe, is entering a long overdue infrastructure expansion and/or upgrade cycle that will certainly be metal- and energy-intensive. A wide range of major water, wastewater, electrical power generation as well as electrical transmission, railroad and bridge projects are either underway or slated to begin in the next few years. But by far the largest driver will be population growth. Today, it is well-publicized that approximately one-third of the world's population lives in countries busy industrializing. Seldom considered, however, is the pace of population growth and the sustained demand that will be generated by the addition of a roughly equivalent number of people in the next 42 years, primarily in the very regions currently under development. It is doubtful this new demand will be anywhere near as intense per capita as that in the US and OECD countries, but the sheer numbers involved are troubling when put in the context of the supply picture. To put these numbers in perspective, each represents approximately 2.5 billion people, which was roughly the entire human population in 1950 or eight times today's US population.

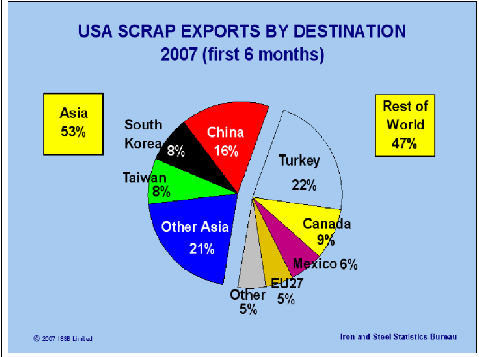

It appears unavoidable then that the demand for… everything will increase accordingly. In fact, according to the National Science Foundation, there is some question regarding whether the planet has the carrying capacity to support a global population in excess of 9 billion at all, let alone a level approaching the lifestyles enjoyed in the US and OECD-- "even (with) the full extraction of metals from the Earth's crust and extensive recycling programs." To the ETR then, the equation looks like this: increased production costs plus reduced supply plus sustained demand, compounded by unprecedented monetary inflation, equals higher energy and commodity prices well into the future. This bodes well for existing ETR themes as well as underpinning this quarter's focus on base metal recycling, specialty metal toll refining, tailings reprocessing and improved process efficiency, for there is a direct correlation between energy and commodity prices and these industries. Detail 3: "We need to minimize waste, find substitutes where possible, and recycle the rest." Despite all of the blather about carbon footprints, saving the environment, and healthy lifestyle choices, doing our bit to conserve resources for most Americans extends little farther than obeying local ordinances that mandate the separation of aluminum, glass and newspaper from our household trash for curbside pick-up. Many of us find recycling and the scrap industry distasteful and tend to dismiss them out of hand. When we think about them at all, we tend to assign both the same stigma we might to hand-me-down clothing or knock-off jewelry. The ETR would like to point out that as strange as it may seem, the scrap metal industry is green. Further, in an effort to dispel a few misconceptions about recycling and the scrap industry, both have long made important contributions to the US economy-one the ETR submits will play an expanded role in the years ahead. Metal recycling has been practiced for millennia, but with the development of the blast furnace in the latter part of the 19th century scrap metal assumed a new role. As the volume of metal production soared, it was discovered that recycling the increased scrap metal waste back into the furnace as secondary feedstock resulted in substantial energy savings. This is because the application of heat returns metal to its basic elemental structure, meaning there is little difference between metal made from fresh ore or recycled scrap. In fact, it turned out that there was little to be gained by preferring freshly processed ore over scrap as mill feedstock but much to be lost in terms of energy consumption, for by reusing scrap metal a mill bypassed the most energy-intensive step in the production process: the conversion of ore to metal. According to the Environmental Protection Agency (EPA), today using recycled iron and steel as feedstock in new production results in energy savings of 74% over production from raw iron ore; recycling copper results in 85% energy savings; and using recycled aluminum saves 95% of the energy required to produce a similar amount from bauxite ore. Few realize the global scrap metal market now exceeds $160 billion in annual sales, of which the US accounts for $65 billion, or that in 2004, a year in which the global steelmaking industry produced more than 1 billion tons of new steel products, scrap metal constituted nearly half of the feedstock. When put in the context of America's vast production and consumption of metals, scrap accounts for "more than half of U.S. metal supply by weight and roughly 40% by value." To get an idea both of how energy intensive metal production is and how much energy is saved by recycling scrap metal, consider: in the case of steel alone, in 1999 recycling scrap saved the energy equivalent of the electricity needed to power about 18,000,000 American homes for one year. The punch line is this makes scrap metal recycling a sustainable, infinitely renewable resource that conserves in-ground reserves. The energy savings further constitute tremendous reductions in greenhouse gas emissions. And recycling diverts millions of tons of materials each year away from landfills and puts them to productive use. All in all, pretty 'green' for a 'smokestack' industry. These energy savings will be increasingly important in the years ahead because the nature of mining is such that the richest ore bodies are always those exploited first. They were the easiest to find, the cheapest to transport, and the least expensive to process. With time, however, as the richest concentrations play out, the overall quality of ore deteriorates. Using iron as an example, in the US the percentage of iron per ton of ore has decreased from 60% during World War II to the vicinity of 25% today, which has increased all aspects of extraction and processing costs, especially energy costs. Interestingly, in 2006 the US utilized less than half of its 140 million tons of annual ferrous scrap metal processing capacity. This suggests the industry is well-positioned to step up scrap production in response to diminished mine production or supply interruptions in the years ahead, which will be critical if we are to achieve so-called resource equilibrium, the point at which recycling existing iron scrap by and large replaces mining. In an industrialized economy, it is widely believed it is possible to arrive at a level of development beyond which only incremental additions of iron are needed in response to population growth and upgrade cycles in order to maintain a desired level of output. Between 1900 and 2004, the US produced approximately 3.2 billion metric tons of iron, the majority of which is still in use and will be available for recycling at some point in the future in much the same capacity mines have traditionally played. It is thought the natural end-of-life replacement cycle of old infrastructure, factories, bridges, railroads and the like as well as the on-going supply of metal from rolling stock-some 14 to 17 million cars and trucks each year, will be able to supply the vast majority of our needs in the future. BRIC industrialization has been the driving force behind five straight years of progressively higher iron ore prices, which in turn has put US scrap metals in high demand. This sustained demand has resulted in US stocks of scrap metal being the lowest since World War II. This is likely to remain the case because until a country reaches a certain level of development and maintains it for a period of time, there are relatively few existing metal-containing structures to demolish or automobiles to dismantle, so it lacks the sheer volume of metal to form the basis for a significant domestic scrap metal market. With some investment banks forecasting a 30- 50% increase in iron ore prices in 2008, China in particular will be looking to the scrap market to supplement its supplies. And the quality of the steel the US produces makes its scrap a much sought-after commodity in its own right (please refer to the chart below). Ironically, the Chinese are huge buyers of US scrap metal in large part because the quality of the scrap metal we sell them as feedstock for their mills is often of better quality than that they would otherwise be able to produce without it.

Source: BIR Elevated prices have also driven a wave of consolidation in the scrap metal industry. Traditionally fragmented with relatively few publicly traded companies, the scrap business has always been highly proprietary in nature, relationship-based, and conducted by people with highly specialized skill sets. For example, a mere glance at the "Scrap Specifications Circular 2007" reveals more grades of ferrous metals than most of us knew existed: there are more than three dozen categories just for railroad scrap. Consolidation within the space is bringing more capacity into the public domain, driven by companies striving for the economies of scale as well as a determined effort on the part of steel mills to increase their exposure to the scrap side of the industry. However, low stocks of scrap material combined with more competition for what is available will likely result in reduced profits for a time, so the ETR urges readers to exercise patience in terms of entries. Also, if a carbon tax or trading scheme is eventually put in place, scrap operations may well represent a source of carbon credit for steel mills, adding fresh impetus to the wave of consolidations. Assuming central bank reflation efforts are successful, any combination of the unintended consequences explored earlier in this report will have a positive impact on the scrap industry. First and foremost, the market will turn its pragmatic eye on expanding existing secure resources and developing technologies to improve recovery rates. The scrap industry stands ready to accommodate increased rates of metal recycling -and there are certainly opportunities to improve:

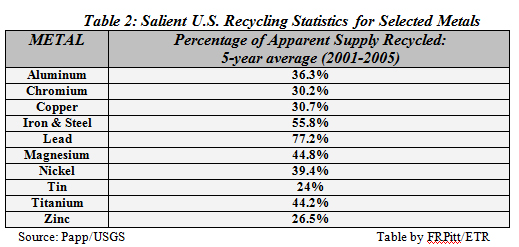

It is likely that continued high metal prices will serve to attract increased public sector recycling, which will help increase the levels in Table 2. It should be noted, however, that because of uses that are dissipative in nature, such as the loss of zinc attendant to galvanizing steel, or otherwise simply impractical to put into effect, few of the recycling rates listed above will ever approach that of lead, which is a special case. That is not to say that in most cases the rates cannot improve substantially for they clearly can and we submit they will, but the case of lead is somewhat akin to that of rhodium in that the former's lead acid battery recycling and the latter's use in automobile catalytic converters is mandated by law--and there is no substitute for either. Although generally regarded a more pressing issue for specialty and precious metals (please refer to Detail 4) than for base metals, the idea of there being limited supplies of, and perhaps no substitutes for, certain base metals has serious implications for global markets. For example, at the current rate of consumption, which is accelerating, of the ten minerals in Table 2 it is estimated the planet has enough copper to last for another 61 years; enough lead for 42 years, for which there is presently no substitute; enough tin for forty years; and enough zinc 46 years, also for which there is presently no substitute. A National Academy of Sciences study on the subject concluded (emphasis added): "…it is clear that, as the proportion of the stock of ore remaining in the lithosphere diminishes relative to the stock-in-use and the stock dissipated, scarcity value will indeed eventually raise the real prices of the geochemically scarce metals and will stimulate intensive recycling well above today's levels. We anticipate that price increases are unlikely to trigger a lower rate of increase in metal services or sudden economic disruption." The Emerging Trends Report is suggesting investors "go to where the puck will be," for the US is uniquely positioned both to expand its use of these low cost, energy efficient, secure methods of meeting its base metal needs as well as to take the lead in demonstrating for the world a conservation model of what is possible in the years ahead. Scrap in the Time of Scarcity is intended to present an enduring evaluation of four sectors that stand to benefit greatly from the ongoing energy and commodity supply constraints the Emerging Trends Report sees continuing for at least the next decade. 60 pages of documented research including 3 original tables and 7 charts cover:

To purchase Scrap in the Time of Scarcity as an individual report, or on an annual subscription basis, we invite you to visit our website at: http://www.emergingtrendsreport.com Richard Karn/Emerging Trends Report January 14, 2008 (510)962-5021 |

| Home :: Archives :: Contact |

THURSDAY EDITION July 23rd, 2026 © 2026 321energy.com |

|