|

MONDAY EDITION March 16th, 2026 |

|

Home :: Archives :: Contact |

|

|

Getting More for LessPeter McKenzie-BrownEmail: pmbcomm@hotmail.com languageinstinct.blogspot.com January 30, 2009  Making a buck in North America’s most expensive gas basin. This article appears in the February 2009 issue of Oilweek. North America’s natural gas business is going through fundamental change, but Alberta’s conventional gas sector isn’t well positioned to compete. As Canadian Natural Resources' president Steve Laut told a conference call when he was discussing his company’s deep cuts in capital spending for 2009. “We are drilling (for gas) in B.C. but cutting back in Alberta. The oilsands can withstand (Alberta’s) higher royalties, and on the oil side, the government got it right, but they missed it on gas. Alberta is the worst place for gas development in North America, and likely the world.” Why are things so bad? Part of the problem is the province’s much-maligned new royalty regime, which sapped the industry’s motivation to invest in the province’s traditional source of supply, conventional gas. In November the province gave explorers the option to pay royalties at the old rate for four years, provided the wells were more than 1,000 metres deep and spudded after the New Year. This eleventh-hour tinkering “will have an improvement on activity levels in the province,” according to Tristone Capital vice president Cristina Lopez, “but it will not improve the cash flow outlook for companies that are going into a difficult commodity-price environment.” That’s a major reason for the decline in conventional exploration and development.

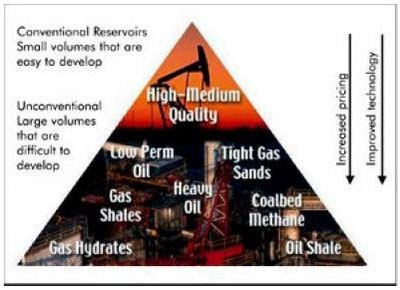

“There’s been a tendency to assume that as long as we have gas opportunities in Alberta, people will come here to invest their money to get it out,” said Dave Russum, who is head of geosciences at AJM Petroleum Consulting. “We should not automatically assume that will be the case. When you change the royalty system and make other such changes, then investors will go to other opportunities where they have other advantages – closer to markets, or where there’s a better royalty regime or a lower cost structure.” He notes that until this year there has been an absolute correlation between wells drilled and gas prices: When prices went up, so did the number of wells. This year, prices went up but drilling in Alberta went down. Was this an unintended consequence of Alberta’s new royalty regime? Probably, but other economic factors are also at play. Geological targets are changing; costs and prices are fluctuating for reasons that have nothing to do with natural gas activity levels (think oilsands); new technologies are fundamentally changing the economics of development; and issues related to environmentally responsive, full-cost accounting are playing an increasingly important role in project approvals. A Fourth Amigo...Again Three Western countries – Norway, Canada and the Netherlands – are now self-sufficient in natural gas (the UK was among them until four years ago). Soon, another country could join that small but lucky band. If you were to hazard a guess, which country do you think might join that group? That country, whose conventional gas production peaked in 1972, began focusing on unconventional natural gas in the 1980s. Today, the Lower 48 states are producing gas at rates near their 1972 peak. Increasing supplies from unconventional gas fields and coal-bed methane are outstripping by far the decline from conventional sources, and LNG production from Alaska is possible. A number of commentators have suggested that these factors could soon make the United States again self-sufficient. An obvious implication is that Canada must develop alternative markets to help create price security. According to Russum, only six percent of the sedimentary rock in the Western Canada Basin is prospective for conventional natural gas. However, the bulk of the other rocks are prospective for biogenic gas, tight gas, fractured gas or shale gas. Coal bed methane represents a tiny additional wedge on his pie. This gas-prone basin, where conventional gas production is in decline, still hosts huge volumes of undeveloped hydrocarbons. That’s a point worth remembering. The cost of developing and delivering Western Canada’s gas varies greatly from region to region, but the WCSB is still one of the world’s most expensive onshore basins to develop. A recently released National Energy Board map illustrated the geographical diversity in cost related to developing and producing these gas supplies. The average cost of gas supplies ranges from $11.18 per thousand cubic feet in the BC Foothills to $6.58 per thousand in the adjacent Alberta Deep Basin. For gas producers and analysts, the critical factor in the NEB analysis was that gas prices need to average $7.88 per thousand cubic feet for producers to generate a risked after-tax rate of return of 15% in this basin. Given an average Alberta spot price for natural gas around $6 during 2007, the report intoned, “the average economics for new gas development in western Canada were marginal.... These results are consistent with the general impressions expressed by industry players about the tight economics of new gas....” Costs and Prices: If the economics are as bad as this NEB report suggests, why is a fair amount of gas exploration even taking place? According to University of Calgary economics professor Robert Mansell, “It depends on your outlook on prices. If you look into the future and you see average prices in the future at $12, say, then you want to establish a position in that play. Even if you think gas prices will never go above $8, you may want to establish reserves at today’s costs. You could sell them to people who have expectations of higher prices.” It’s all about price and cost. Even though unconventional gas is more expensive to develop than conventional production, that’s where about 60% of natural gas activity is going. Like the US, which made great progress developing unconventional gas during an era of lower prices, Western Canada is developing these resources in a period of price/cost disequilibrium – that is, lower prices and higher costs. This is counterintuitive. In classical economics, adversity in the gas industry – the lower margins and riskier business environment of the last few years, for example – would force the industry to drive down costs and increase efficiency. The U of C’s Mansell squelched that assumption, first zeroing in on the dynamic relationship between price and cost. “Costs drive prices,” he said, “but prices also drive costs.” Supply costs go up and down depending on activity levels, rig and services availability, materials, labour, technology, changes in well productivity, changing drilling targets, and changing fiscal and tax regimes. Crown land prices go up and down as well. The main way the recent downturn would force the gas industry to become more efficient, said Mansell, would be through consolidation. “In this environment, there’s likely to be much more rationalization.” As smaller companies combine into larger ones, they generally become more efficient. Technology: While companies employ cost-cutting measures (shutting in higher-cost gas supplies during tough times, for example), Mansell makes the case that real efficiencies are more likely to arise in periods of relative prosperity than in periods of economic adversity. “In a tight margin environment, would companies put more R&D and technology into increasing efficiency? It’s not clear. They actually have more free cash to play with in a higher price environment (and are therefore in a better position to increase efficiency). However, if a company is financially healthy, it can even increase profits in a low-cost environment by applying new technologies.” In other words, greater efficiency in the petroleum sector comes mostly from technology –improved drilling, seismic and other technologies used in exploration and development – along with the obvious benefits of such capital infrastructure as plant and pipeline. According to Mansell, “It’s a dynamic environment. Mostly because of better know-how, over longer periods of time the industry is getting 1.5% to 2% more output per unit of input each year.” How is that happening? AJM’s Dave Russum puts a technical slant on things. “Per well costs are higher than in the past, that’s true. However, we now understand that in certain kinds of gas resources we can greatly increase productivity by increasing drilling density in lower-quality gas reserves. You need to be able to fracture the maximum amount of the reservoir.” So important has this trend become that it is contributing directly to the reduced number of wells being drilled in Canada. This year, nearly 40% of the wells drilled in Canada will involve horizontal or directional drilling – twice the level of ten years ago. For the first time, First Energy Capital said in a recent research note, the number of horizontal wells will match the number directionally drilled, and more and more of well costs are in completion technology. Fracturing consists of injecting a fluid into a well to cracks or fractures already present in the formation and create new ones. Russum is especially keen on combining and the use of multi-stage fracturing techniques prior to completion of horizontal wells. “Between the heel and the toe of a horizontal well,” he says, “you can isolate an interval close to the toe, frac that region, then move back towards the heel, isolate another interval and do another frac. This breaks up a lot of rock, and makes a lot more gas available. These new technologies are enabling us to access a whole lot more low-permeability rock than you would ever be able to reach with a vertical well.” As the U of C’s Mansell points out, “Current costs may not reflect future costs. As you learn more about the resource, costs could come down substantially – not only the cost of production, but also the cost of finding new reserves.” Recent innovations in fracing wells illustrate how this can happen. Companies have made great strides in increasing the number of fracs they can make in a single horizontal well. Horizontal wells drilled into shale reservoirs now average eight fracs each – an astonishing improvement from only ten years ago, but one that is causing potential bottlenecks in the system. According to Kevin Lo of FirstEnergy Capital, to fracture just one of the Horn River shale gas wells in north-eastern BC, you need a fracturing crew equipped with more than 30,000 horsepower of compression. To put that in perspective, in Western Canada perhaps 800,000 horsepower is available. “We do not believe that there will be sufficient capacity to perform all of the jobs necessary, should (BC’s Horn River and Montney shale gas) plays grow,” he said in a research note. He also worried about the logistics of bringing in enough propping agent: fracturing a single horizontal well in these reservoirs can require up to two thousand tonnes of sand. Stewardship: Another area where big changes are happening, of course, is in environmental practice and policy. Take the case of EnCana’s application to drill in the Suffield National Wildlife Area, where a hearing began last September. The gas at Suffield is shallow, biogenically-derived gas in mixed sand and shale sequences. Since it is not generated in the same temperature and pressure systems that create conventional hydrocarbons, shallow biogenic gas is an unconventional variety. The Milk River and Medicine Hat sands of south-eastern Alberta and south-western Saskatchewan are classic examples of this type of unconventional gas. This was the first gas produced in western Canada. It is continuously gas-producing, and it is the largest gas-producing region in the WCSB. For efficient production of biogenic gas in this area you need close well spacing, and you generally can’t use horizontal drilling because the wells are so shallow. Developing production in these fields is almost like assembly-line manufacturing. You haul in a small rig on a system that causes minimal surface disturbance, drill and complete the well in a day. You can use nitrogen and CO2 fracs, which reduce environmental damage in really shallow wells. Then other crews come along, install the wellhead and tie production in to a pipeline. Sounds pretty green, doesn’t it? Not according to the Alberta Wilderness Association’s Joyce Hildebrand. “Extracting resources is only one of the mandates of the government, whether at the provincial or federal level,” she says. “Another mandate given to the government by citizens of Canada and Alberta is to set aside environmentally significant areas so that they are off-limits to human activities, such as oil and gas exploration, that may compromise their natural values; to preserve species that have been designated as endangered, threatened or otherwise at risk, and to preserve the habitat that those species depend on.” She adds, “The evidence is overwhelming that doubling the number of wells, and constructing the necessary associated infrastructure such as pipelines and roads, in the Suffield NWA will seriously compromise the habitat of (species at risk). If the habitat goes, the species go. So as a society, we need to decide whether we want to sacrifice the conservation of that endangered prairie ecosystem for the acceleration of the resources under the ground. Those two choices are incompatible – it’s one or the other. There is no possibility here of ‘balancing’ the two….The sooner we begin to work on a macroeconomic policy that is based on something other than the well-funded rhetoric that economic growth and conservation of wilderness is compatible, the better. The situation at Suffield is one example where that needs to be challenged.” The issues are complex, and the ERCB has a long history of listening carefully to all sides and dealing with these situations fairly. However, this is only right. As the U of C’s Mansell explains, economic theory supports the environmentalists’ point of view. “In theory,” he says, “you want to be as close as possible to full-cost and-full benefit accounting from a social point of view. Policy decisions should incorporate all incremental benefits and the incremental costs – including costs and benefits that don’t necessarily show up in the market. How you estimate that isn’t an easy question to answer, but your accounting should be based on a benefit-cost analysis.” Since a poll by the provincial government found that only 16% of Albertans believe the province does a good job of looking after the environment, this story has legs. So there you have it.

Alberta may be “the worst place for gas development in North America.”

However, the WCSB remains an important gas basin, and activity

throughout the region is helping illustrate gathering industrial

trends. On the policy side, issues related to full-cost accounting will

likely take years to iron out – but at least they are being heard.

|

| Home :: Archives :: Contact |

MONDAY EDITION March 16th, 2026 © 2026 321energy.com |

|