|

TUESDAY EDITION June 9th, 2026 |

|

Home :: Archives :: Contact |

|

|

Asia AscendingPeter McKenzie-BrownEmail: pmbcomm@hotmail.com languageinstinct.blogspot.com January 9, 2008

Royal Dutch Shell traces its origins to Sumatra, and now Canadian companies are on the hunt for similar growth opportunities in Southeast Asia One hundred and twenty five years ago a Dutch planter, A. J. Zijlker, took cover from a tropical storm while travelling on the island of Sumatra. Sheltering in a tobacco shed, he saw a watchman light a fire from wet twigs using a bamboo torch. He asked what was fuelling the torch and the next day was taken to a small pond covered with a dark liquid. Soon after, Zijlker drilled the Telega Tila oil well near that pool. From his precarious derrick, Royal Dutch Shell's global empire eventually grew. This and other such ventures launched the petroleum industry in Southeast Asia and linked its resources to the energy markets of the world. As a result, Indonesia became a large-scale producer. The other regions of Southeast Asia, however, did not – at least not in the early days. Two world wars, the often bloody collapse of colonialism, political instability and the rise of autocratic government, endemic corruption – all these helped keep the petroleum industry out of the region. On the Southeast Asian mainland things were worse than in the archipelago. Not until after the Indochinese war did the area develop the stability needed for large-scale exploration and development programs. Pan Orient: Fast forward to the present, and the Calgary offices of Pan Orient Energy. Everywhere you look there are Southeast Asian artefacts. The company’s offices are adorned with paintings of Buddha, a wooden sculpture of one of the ferocious demon-guardians that embellish Thai temples and many other fine pieces of traditional religious art. And so it should be. One of few Canadian companies willing to risk operating in Southeast Asia, Pan Orient has achieved considerable success in Thailand.  According to Pan Orient’s president, Jeff Chisholm, Southeast Asia is an ideal place to do business. The “real story” about the region, he says, is that smaller companies coming even into the heavily explored parts of Southeast Asia can succeed. “When the region was drilled in the ‘70s and ‘80s, the development threshold was a field of 50-100 million barrels” because prices were so much lower. Today, “we can make a lot of money on a 10-million-barrel field.”

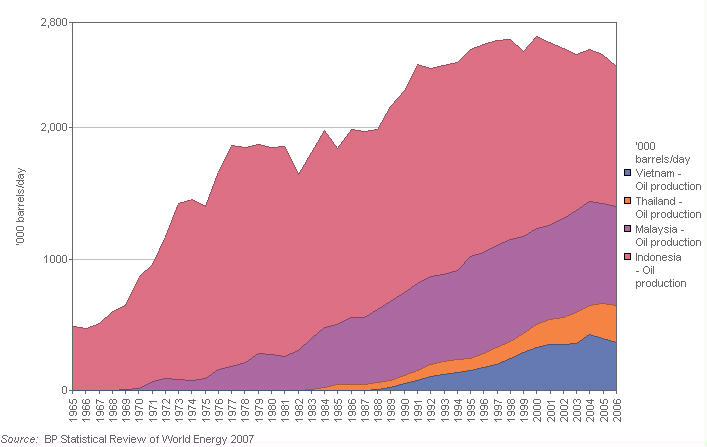

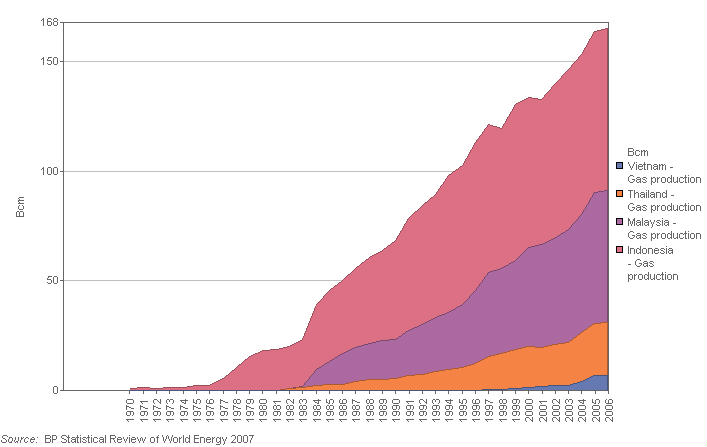

According to Pan Orient’s president, Jeff Chisholm, Southeast Asia is an ideal place to do business. The “real story” about the region, he says, is that smaller companies coming even into the heavily explored parts of Southeast Asia can succeed. “When the region was drilled in the ‘70s and ‘80s, the development threshold was a field of 50-100 million barrels” because prices were so much lower. Today, “we can make a lot of money on a 10-million-barrel field.” Although Pan Orient hasn’t done enough drilling to be able to calculate total reserves at its new onshore discovery in central Thailand, the first four wells tested between 1,200 and 1,900 barrels per day from multiple zones, and the company plans to complete another six wells. Chisholm, who has spent most of his career as an explorationist in South and Southeast Asia, is sanguine about drilling in the region. Are there major political risks? He doesn’t think so. “The Asian economies are growing fast, so the governments need to keep the economy going. That means they need more (domestic) oil production.” Also, they learned from the 1997 currency crisis that they need to “keep their markets open, impose better financial controls and reduce corruption.” In the region, only Indonesia has recently made changes to its fiscal regime. The country made its industry more attractive to foreign investors because the vast archipelago – formally a member of OPEC – has become an oil importer. Still poor, the government desperately wants to produce more oil. Chisholm says Thailand, with its open-bid system, is the most straightforward country to get into. The country has land auctions every two years. The government opens up areas of “deemed prospectivity,” and asks for bids. To participate, you submit two envelopes to the Department of Natural Resources. The first describes your company’s credentials and financial information. If you get past that hurdle, departmental experts open the second envelope and review your proposed work program. To be awarded the contract, you must pass both tests, but it can take time. In the case of Pan Orient, the company worked with the elected government of Thaksin Shinawatra for more than a year to resolve some regulatory matters, with no success. The delays ended quickly after a military government took over in a bloodless coup, however. Chisholm offers this as evidence of the virtual irrelevance of political issues for explorers operating in Southeast Asia. What about Burma (Myanmar)? “Burma’s about the only place you need to stay out of,” he says. “If the UN tells us it’s a bad place, we’ll take their word for it.” End of story, almost. As two Canadian companies discovered to their cost, you can pay public relations penalties for failing to heed Chisholm’s advice. Oracle Energy Group and CHC Helicopter Corporation both announced plans to conduct petroleum-related work in Myanmar, and both soon found themselves demonized on the Internet. The Burma Campaign UK, a human rights organization opposed to the brutality of that country’s military regime, has posted the particulars of each company on its “Dirty List” of businesses that have signed contracts with the generals. There are numerous petroleum basins in Southeast Asia, many of them world-class. According to the United States Geological Service, 15 per cent of the world’s undiscovered oil and gas resources are in Southeast Asia. That prediction is an expert guess from an expert source, but proof can only come from the ultimate lie-detector, the drill bit.   Another way to illustrate the region’s potential is to look at recent changes in production. The charts show oil (top chart) and gas production from the four largest Southeast Asian producers: Indonesia, Malaysia, Thailand and Vietnam. As they illustrate, growth in gas production since the early 70s has been rapid – indeed, this region has the world’s fastest-growing natural gas markets. In addition, growth in oil production outside the aging fields of Indonesia has also exhibited considerable strength. Most of the other countries of the region – Brunei, the Philippines, Papua New Guinea and blackballed Burma – also have exploration potential and expanding, lower-cost production. Talisman: Though only a handful of Canadian companies are active in Southeast Asia, their experience has been positive. As we have seen, Thailand has been the key to success for Jeff Chisholm’s Pan Asian Energy. Two of Canada’s heavyweight producers – Talisman Energy and Husky Energy – also have interests in the region.  Talisman is the larger and more experienced of the two. According to vice president Jonathan Wright, the region has world-class production basins, low-cost operations and, because of the terms of the production sharing contracts his company has signed with the resource owners, rapid return of capital. For its part, the company has large and growing exploration acreage in the region, and existing production.

Talisman is the larger and more experienced of the two. According to vice president Jonathan Wright, the region has world-class production basins, low-cost operations and, because of the terms of the production sharing contracts his company has signed with the resource owners, rapid return of capital. For its part, the company has large and growing exploration acreage in the region, and existing production.The company got its foot in the door in the early 1990s when Talisman took over Bow Valley Energy, which had concessions in Indonesia. The jewel in the company’s Indonesian crown is the Corridor property on the island of Sumatra, where the company has a huge gas field still being drilled, and still not fully understood. According to Wright, the reservoir is unusual in that it is not in sedimentary rock. “It is a basement granite structure. The reservoir is extremely porous and permeable, but the porosity exists mainly in fractures in the granite.” Some of those fractures are kilometres in length. With its 2001 takeover of a Swedish company, Lundin Oil, Talisman added properties in a border area between Malaysia and Vietnam to which both countries had previously laid claim. The two countries reached an accord by agreeing to share production and called it the PM3 Commercial Arrangement Area, and Talisman is now partnering with national oil companies Petro-Vietnam and Petronas. Production is underway, and the three partners are investing more than $1 billion to expand production via the Northern Fields Project. They expect to nearly double production from its present daily rates – 40,000 barrels of oil and 175 million cubic feet of gas. Talisman’s share is 41 per cent. Southeast Asia already accounts for nearly 25 percent of Talisman’s total production. This is an especially impressive achievement when you consider that the company’s reserves have grown steadily and greatly since 1992, when the company became an independent entity. (Up to that time, it had been the Canadian subsidiary of BP.) Talisman’s main production Southeast Asian production comes from Malaysia and Indonesia. The company has already announced exploration successes in Vietnam, however, and expects that country to be another good growth area. The company’s regional headquarters is in Kuala Lumpur, where Jonathan Wright hangs his hat. Few people are more enthusiastic about the region’s high potential than Wright. “Costs are rising here,” he says, “but they are still low compared to the rest of the world. And Vietnam and Malaysia are among the lowest-cost areas” per barrel for offshore exploration. “There are good hunting grounds here, but you have to be selective.” In Malaysia the shallow basins have already been explored, “so you have to go (into) deeper (waters) or tie back smaller fields.” By contrast, Vietnam has not been as heavily explored, and the opportunities there are considerable. In one of its concessions, Talisman has been the beneficiary of two new-field discoveries. The first, which Talisman operated, may have 70-100 million barrels in place. The second is an industry discovery with perhaps 200-300 million barrels in place. Unfortunately for Talisman, only a small portion of the field lies on the block it shares with its partners. “In our opinion (the contract area now being explored by Talisman) is the best block recently awarded in Vietnam,” says Wright. “It has basement granite as well as (more traditional sedimentary reservoir) potential. With luck, our Southeast Asia production could eventually rival our production from the North Sea.” Talisman is also pursuing exploration properties in Papua New Guinea, where it has already acquired natural gas acreage; in Thailand; and in the South China Sea offshore southern China. Technically the latter is not Southeast Asia but, says Wright, “geology knows no boundaries.” Operations: Husky Energy must agree. The company has successfully secured exploration holdings off the coast of China, but the operator is a Chinese company, not Husky. The company has also negotiated a production sharing contract in the Madura Strait offshore Indonesia. Its contract area contains two prospects which, the company says, offer significant exploration promise. The only large Canadian company besides Talisman now present in Southeast Asia, Husky describes its entry as part of a strategy to discover and develop conventional oil and gas outside North America. Do Canadian companies operate elsewhere in the world to the same high standards expected of them in Canada? According to Talisman’s Wright, the answer is a slightly qualified “Yes”. “Our environmental standards are the same (across the company) because we are one company,” he says. However, “the rules are different in different countries. We have to follow local regulations.” In Alberta virtually no natural gas can be flared. In the North Sea and Southeast Asia offshore, however, flaring is “permitted within certain limits, as there are sometimes no economically viable alternatives.” With that qualification, Wright says, “our health, safety and environment umbrella is similar around the world. Our effluent standards for discharged water are the same in the North Sea and offshore Vietnam.” Is operating in Southeast Asia difficult from either a technical or a cultural perspective? Both Pan Orient’s Jeff Chisholm and Talisman’s Jonathan Wright say it isn’t so. According to Chisholm, “one key to successful operations is to incorporate as many locals into the work as you can.” Adds Wright, “you have to turn yourself to the national culture and setting. Beyond that, exploration challenges are similar around the world.” Both Pan Orient and Talisman have demonstrated that developing a production base in Southeast Asia makes business sense. The pity is that other Canadian explorers haven’t yet taken that path. Fiscal Issues in the Region: Southeast Asia is a region of vast diversity. Its countries host more than a thousand distinct languages and even more ethnic groups; a jumble of local customs, traditions and beliefs; and half a dozen major religions. The nations of this region have numerous forms of social organization, and they are ruled by governments ranging from monarchy through an assortment of democracies and socialist republics to Burma’s wicked military regime. For all their variety, these countries have one thing in common. In each case, the central government claims ownership of petroleum resources. Also, they have similar royalty regimes. Foreign companies gain the right to operate by signing technical assistance contracts (TAC) and production sharing contracts (PSC). Technical Assistance: Technical assistance contracts are for marginal discovered fields that need technical help. One Canadian company that has secured such a contract is Vital Resources Corp. Vital’s technical assistance contract covers two properties – the Ramok and Senabing oilfields. The fields were discovered in the early 1900s but abandoned for decades until production was restored earlier this decade. According to the company’s Mike Whitehead, the TAC includes provisions that its costs will be paid out first from future production. After payout, the company will receive 30 per cent of gross production. What is the potential for these fields? At present, they produce barely 100 barrels per day. If Vital is successful with its proposed $6 million enhanced oil recovery scheme, production could ramp up to as much as 2,500 barrels per day. For a micro-cap start-up like Vital, this contract could be the company-maker. Production Sharing: Production sharing contracts are for areas that are prospective, but where there are no producing fields. While the specifics differ from country to country, the basic deal is the same. The country provides the contract area (prior to the 1970s, known as a “concession”) and may choose to put up some of the capital in return for an equity position in any discovery. The operator, however, develops the play and provides its own share of capital and the expertise needed to find and develop any hydrocarbons present. Royalties vary, depending on whether capital investment has been recovered. Before the project has paid out, the royalty is based on “cost oil”, and it is small. Until the investors have received full payout, the company pays a royalty of, say, 10 per cent to the host government. This enables the investor to quickly recover the cost of successful drilling programs. After payout, production is known as “profit oil”, and the royalty increases. In the case of Pan Orient Energy, the company will pay the Thai government a production royalty of 15 per cent of profit oil, in cash. The company will also pay a 50 per cent tax on net income. The Size of the Prize: In terms of economics, how does petroleum production in Southeast Asia compare to production in Canada? It’s hard to put the two side by side, but Talisman Energy vice president Jonathan Wright provides a ballpark estimate. “In Malaysia, the industry take (revenue share after expenses, royalties, and taxes) is 17 to 20 per cent (depending on the mix of oil and gas production). In Canada it averages about 25 per cent.” The gap between the two countries probably narrowed with Alberta’s recent royalty changes. Furthermore, he says, “The size of the prize is much greater here in Southeast Asia. Multi-hundred million barrel fields are still being found, in deeper horizons.” No such fields are likely to exist in Western Canada anymore. Peter McKenzie-Brown Email: pmbcomm@gmail.com languageinstinct.blogspot.com January 9, 2008 |

| Home :: Archives :: Contact |

TUESDAY EDITION June 9th, 2026 © 2026 321energy.com |

|