|

TUESDAY EDITION June 9th, 2026 |

|

Home :: Archives :: Contact |

|

|

Free UraniumBy Alf Field July 13, 2007 www.freebuck.com In January 2006 I published an article entitled "Another Free Call Option on Uranium". The

company concerned has developed to the point that it now represents "Free Uranium!" The original article

can be accessed at: The company concerned is Compass Resources (CMR on the

Australian Stock Exchange). The following was the reasoning for being bullish

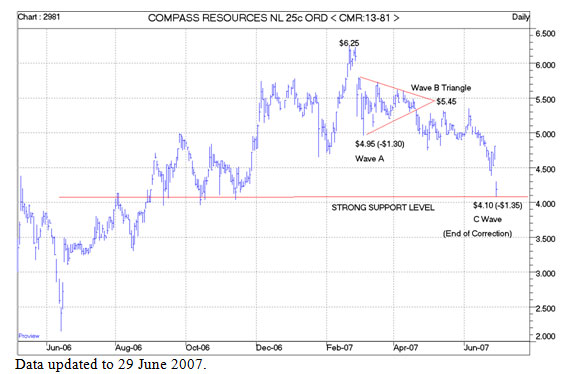

on this stock 18 months ago: Subsequent events have been positive for CMR. The CMR share price at the time of my last article was A$1.50. It has since advanced to a peak of A$6.25 in February 2007 and then declined in a correction that appears to have ended on Friday 29 June 2007 at A$4.10 in a high volume (10.5m shares traded) panic sell-off. The reasons for this sell-off are set out in a separate section below. The following chart depicts the CMR share price action over the past 15 months.

The panic sell-off seems to have bottomed at a strong support level just above $4.00 and the shape of the correction is a completed A-B-C Elliott Wave consolidation where the A-wave and the C-wave are of similar dimensions (-$1.30). What is important is that technical analysis suggests that the correction since the $6.25 February 2007 peak is probably over. This is a good buying point from a technical point of view. Despite the CMR share price tripling over the past 18 months, an investment in CMR can now be regarded as "Free Uranium". This is explained separately below. In addition CMR shareholders will receive a "free lottery ticket" on some exciting base and precious metal exploration projects in an under-explored area of Australia. Before proceeding to the detail of why this is the case, let me firstly declare my interest in CMR. I bought CMR in early 2005 at 60c, making additional later purchases at $1.03 and at $1.28. I sold about a third of my position during the recent strong run up in the CMR share price. Thus I have recovered my total original cost and banked a decent profit. During the panic sell-off on Friday 29 June 2007, I took the opportunity to buy back (at $4.24) some of the CMR shares sold at higher levels. My intention is to retain my position in CMR until the company is fully mature. I have no business relationship with CMR, other than being a shareholder, and have not been paid nor received any other inducement to write this article. The bottom line is that I am not a completely independent, objective, observer and am obviously biased in favour of the company. Anyone contemplating an investment in CMR should conduct their own due diligence on the company.

Achievements during the past 18 months:

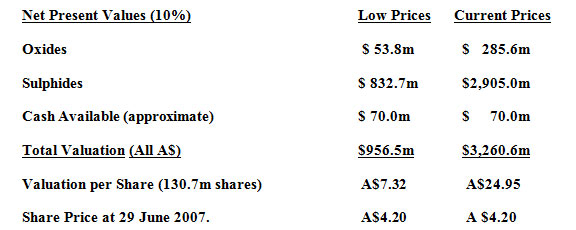

Valuation of the Browns

Oxides and Browns Sulphides projects:

The Low Prices estimate included metal price forecasts as follows: Copper - US$3.13 lb declining to $1.50; Cobalt - $12.50 throughout (currently over $30 per lb); Nickel - $10.75 down to $4.50; (currently $16.00lb); Lead - US$0.35 throughout (currently about $1.20!). Current Prices Estimate (as at 10 May 2007) - used the following metal prices throughout: Copper - US$3.72; Cobalt $30.50; Nickel - $24.00; Lead - $0.94c.

There is no doubt that the company's calculations are likely to be more accurate than an outside analyst's best guess, so I am happy to rely on these calculations for purposes of this report. The above calculations show that the most influential input factor or variable (as with all base metal investments) is the level of future metal prices assumed. CMR is very highly geared to the future level of metal prices. If metal prices do decline severely to the levels assumed in the Low Prices estimate, the NPV is still well above (in fact 75% above) the current share price of $4.20. If future metal prices are anywhere closer to current levels, CMR is worth multiple of the current $4.20 share price. My personal opinion is that future metal prices will exceed the recent high levels due to:

It is unlikely that anyone's opinion on future metal prices will be lower than the Low Prices estimate used above. That being the case, CMR is greatly undervalued at $4.20 per share, based only on its two base metal projects and using the most conservative of metal price assumptions. That means that the company's other assets, specifically its uranium assets and 100% owned exploration projects come free and clear to shareholders. Detailed examination of CMR's uranium and exploration assets will follow, but first it is important to deal with the reason for the share price collapsing over 12% last Friday, 29 June 2007, to $4.10. CMR Share Price Sell-off on

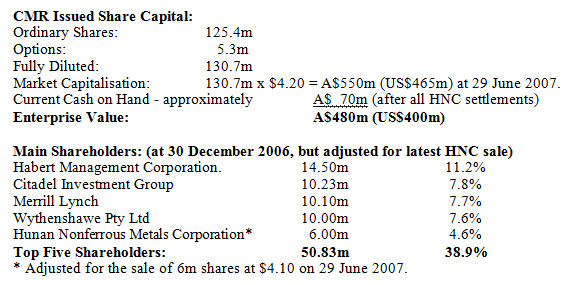

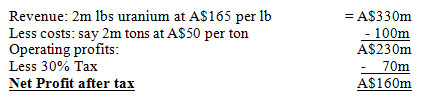

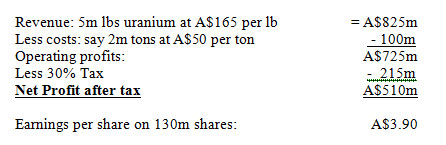

29 June 2007. The market quite naturally made the assumption that HNC had lost confidence in its CMR investment and that they were pulling out of their JV commitments. It seems that this was an erroneous conclusion that the market jumped to. It is necessary to go back to the reason why HNC originally made their investment in CMR shares. This came about because the CMR Chairman, Gordon Toll, advised HNC that he was not prepared to enter into any detailed negotiations with HNC until HNC had demonstrated its bona fides, and indicated that they were serious about the negotiations, by firstly making an investment in CMR. Mr Toll deemed a $30m investment into CMR as an adequate gesture of good faith. This also meant that if the negotiations with HNC fell through, CMR with the additional $30m in its bank account, had sufficient funds to complete the construction of the Oxides plant. Thus HNC purchased 12m CMR shares at $2.50, putting $30 in cash into CMR. HNC was under some duress to make this investment as their corporate strategy is to invest in projects, not in companies. The investment was made purely to show good faith by HNC. Tortuous, long drawn out negotiations followed, with 3 voluminous contracts being drawn up in Mandarin and in English, with multiple lawyers and translators on both sides. Eventually, just a couple of months ago, the 3 agreements were signed amidst much ceremony. Having demonstrated their good faith via the long process leading up to and including the signing of the agreements, HNC obviously felt that they had more than demonstrated the seriousness of their intentions. From the HNC point of view, the $30m that they had placed as a "good behaviour" bond by buying CMR shares, could now be returned. The share price had risen, so they could sell half their holding and recoup most of the $30m, hence the decision to sell their CMR shares. There is no question that the sale could have been handled more sensitively, but that is perhaps the nature of dealing with people from different cultures. The important fact is that there is no indication that HNC is planning to resile from the JV contracts. Thus far they have met their obligations of two $15m payments with a further $10m due on 30 June 2007. The final balance ($42m) will be paid when the NT Government finalises the amount of stamp duty to be paid on the JV contracts. There is no question that HNC are keen to expedite these projects and keen to see a much larger Sulphides project than the original 4m ton per annum plant that has been suggested. That level of production would provide a 20 year life for the project. HNC is paying 70% of the drilling costs on the NT tenements for 5 years with the objective of doubling the current JORC base metal resource base to something approaching 160m tons. That would allow for a larger Sulphide project, possibly 6m tpa or even 8m tpa. It should be noted that if the Sulphide project is expanded by 50% to say 6m tpa, the NPV calculations set out above would also increase by 50%! HNC people will be working very closely with CMR staff on the Definitive Feasibility Study as it will be HNC that will fund the construction of the Sulphides plant. Both sides would like to see the highest possible NPV emerge from the project. It is estimated that a 4m tpa plant would cost A$750m to $800m. Presumably a 6m tpa plant would cost of the order of $1.1billion to $1.2 billion. The importance of these numbers is that if HNC invests funds of this magnitude up front for just 50% of the metal (and 50% of the operating costs), then CMR's 50% of the project should be worth at least the same amount as HNC spends on the plant. This would be added confirmation of the validity of the Sulphides NPV's displayed above. It would appear that the stock market's initial assessment of HNC's sale of CMR shares was incorrect. The decline in the CMR share price represents an excellent buying opportunity. FINALLY - CMR's Free Uranium! It is interesting that in any listing of Australian uranium exploration and embryonic uranium mining companies, the name of Compass Resources is nowhere to be seen. Similarly any world wide listing of companies with known uranium resources fails to mention CMR. This company is well below the uranium radar, but this will change dramatically over the next 6 to 9 months when the CMR uranium section is split off into a separate company and a new uranium JORC resource base is calculated incorporating the last 2 years drilling results. The fact is that 14.5m lbs of resource at less than 1 lb per ton does not excite the speculative juices. Naturally that is not the complete story. It is just the start of the story. What first caught my attention at CMR from a uranium point of view, was the fact that CMR owned all the old Rum Jungle and Whites uranium mine tenements. Rum Jungle was the first uranium mine in Australia nearly 50 years ago when the Atomic Energy Board let a contract for 10m lbs of uranium. The Rum Jungle pit produced about 6.8m lbs at a grade of about 8.5lbs per ton and the Whites pit produced 3.2m lbs at about 6.5 lbs per ton. When the 10m lb contract was completed, the mines closed down. No further work was done on the property as far as uranium was concerned until CMR started exploring on the property a couple of years ago. Rum Jungle did not close for lack of ore. It closed for lack of a customer. The old adage that one should look for new deposits in the shadow of a mine head gear is a sound one. There must be plenty of uranium left in the area around the Rum Jungle and Whites pits, but CMR chose to concentrate on the Mt Fitch area, which is about 15km north of the Rum Jungle/Whites pits. The reason is that they felt that they could very quickly identify a mineable resource, albeit relatively low grade, at Mt Fitch. It is on surface and can be mined easily, conveniently and inexpensively. That is where the initial 14.5m lbs resource is located. Further extensive drilling in the Mt Fitch area, both in-filling and step out, has taken place over the past 18 months and the next JORC report should see this deposit increase both in size and grade. Mt Fitch is an area where permitting should be easier than most. The plan is to construct a 2m tpa uranium plant about midway between Mt Fitch and the Rum Jungle area. Initial mining will be from Mt Fitch but gradually CMR will bring smaller, higher grade pits near Whites and Rum Jungle into production and perhaps half of the 2m tpa will be higher grade material. Thus initial production will be about 2m lbs per annum (2m tons at 1lb per ton). Later half the production will come from the south at grades of possibly 4lbs per ton. This will boost uranium production to 5m lbs per annum, a figure that has been mentioned from time to time, most recent by the Chairman at the AGM on 31 May 2007. As mentioned in the preamble, an independent scoping study was done on the Mt Fitch resource which determined that not only was it economically viable, but had a healthy NPV at 10%. I extrapolated the NPV forward to take account of the latest uranium price of about $140 per lb. At that level the Mt Fitch project has a NPV of $610m. Note that this is in excess of the current Enterprise Value of the entire company of $480 million! To put it another way, the Mt Fitch resource alone more than justifies the current share price - and then all the base metal projects come free! But there is more, much more. We can only speculate at this stage about what the next uranium JORC resource statement will show, but one approach would be to say that CMR hopes and expects to be producing 5m lbs of uranium per annum for 10 years. That requires a resource base of 50m lbs. Is that possible? I don't know, but there have been a number of interesting drill hole results that suggest that it may be. For example, two results published on 15 February 2007 at Browns East (450 metres from the old Whites pit) produced 6.68lbs of uranium over 1m (out of a 10m intersection averaging 2.11lbs per ton); 12.8lbs per ton also over 1m (out of a 10m intersection that averaged 2.83lbs per ton). These holes are in the same area as the old Rio Tinto hole DD137 drilled 50 years ago which intersected 4m of 11.3lbs uranium. These Browns East holes also included good copper intersections of 22m @ 2.43%; 27m @2.09%; and 21m @ 2.55%. Lower grade nickel and cobalt was also found in these holes. This represents very valuable rock. We can now turn to the profit potential of the CMR new uranium company. Using the initial production level of 2m lbs per annum, just from Mt Fitch, and using the current uranium price of US$140 (A$165) provides the following financial results:

A new uranium plant is said to cost about $65m but this estimate may be too low. Assume that the capital cost is twice as much, say $130m. That still means that capital payback period would be less than 12 months, a very healthy situation. The new uranium company should receive say $50m cash from CMR's cash resources, so it will need to either borrow $80m or tap the shareholders for that amount to complete the construction of the new plant. One possible solution would be to issue 2 year options as an attachment to the new Uranium Company shares (will it be called Rum Jungle Uranium Mines?) to raise the necessary capital when it is required. Just by way of example, if the new Uranium company issues 65m new shares (one for every 2 CMR held) plus 65m 2 year options to take up new Uranium company shares at $1.25, that would raise the necessary $80m and leave 130m Uranium company shares in issue after the options are exercised. The options would be traded on the market, thus shareholders not wishing to take up more shares could dispose of their options. Just to complete the uranium exercise, at a production level of 5m lbs uranium per annum, the financials would look like this:

What should be apparent from these hypothetical calculations is that the new shares - let's call them Rum Jungle Uranium Mine shares - should be a valuable commodity when they are issued free to CMR shareholders. The only remaining question is how long it will take to construct the uranium plant and bring it into production? The Chairman at the AGM mentioned 30 months from a standing start, but it may be wiser to allow more time. Some time in 2011 seems a conservative estimate to be in full uranium production. Free Exploration Lottery Ticket. The second "freebie" that will be coming the way of CMR shareholders will be free shares in the new exploration company that will be spun off, which will own CMR's exciting 100% owned exploration targets in NSW and in Peru. As with all exploration companies, this could be a fizzer or it could possibly become a major mining company if it discovers an "elephant" or two (or seven!). What gets red-blooded explorers pulses racing are the tenements that CMR has assembled in western NSW. Four exploration licenses have already been granted and three more have been applied for. If all seven are granted, the area covered would be over 2,000 sq kilometres. Clearly "elephant" country! Radiometric surveys picked up seven seriously large anomalies, which is probably the reason for the additional 3 exploration applications. This is all virgin ground and it is fair to say that some old time geologists who are not given to hyperbole (we know that this company does not even "talk the legitimate talk") are excited about the area. A wild cat hole drilled in the area last October intersected look-alike geology to the established Cobar Basin. Anomalous copper, zinc, tungsten and silver mineralisation was found. Further drilling should start within the next 2 months. Whatever you do, don't throw this free exploration lottery ticket away. SUMMARY CMR is a treasure trove of undervalued goodies waiting to be discovered. The next 6 to 9 months will be an exciting time for CMR shareholders as these values becomes more apparent to the market. The company is also committed to start "talking the talk" and promoting the company internationally. The misunderstanding by the market of the sale of HNC's 6m shares which caused the recent share price decline has created a great opportunity to accumulate CMR shares at favourable prices. Alf Field July 13, 2007 Comment to: ajfield@attglobal.net Disclosure and Disclaimer Statement: In the interest of full disclosure, the author advises that he is not a disinterested party in that he has a personal investment in Compass Resources shares. The author's objective in writing this article is to interest potential investors in this company to the point where they are encouraged to conduct their own further diligent research. Neither the information nor the opinions expressed should be construed as a solicitation to buy or sell this or any stock, currency or commodity. Investors are recommended to obtain the advice of a qualified investment advisor before entering into any transactions. The author has neither been paid nor received any other inducement to write this article. |

| Home :: Archives :: Contact |

TUESDAY EDITION June 9th, 2026 © 2026 321energy.com |

|