|

SATURDAY EDITION July 4th, 2026 |

|

Home :: Archives :: Contact |

|

|

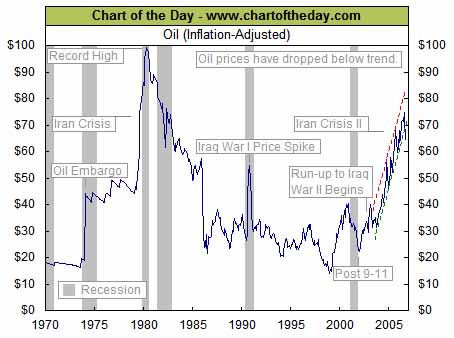

TECHNICAL SCOOPTo Peak Oil, or not To Peak OilDavid Chapman of Union Securities Ltd. www.davidchapman.com September 28th, 2006 We have been struck by the number of bearish reports and comments emanating from analysts, fund managers and assorted pundits with regard to oil, gas and other commodities. Just prior to the release of the FOMC statement on September 19, we heard a well-respected Chicago floor trader gush about how the oil bubble had burst, and how the Fed wouldn’t need to hike interest rates any further. Hearing that, we were tempted to rush out and trade in our 35 miles per gallon Honda for a gas-guzzling SUV as we watched prices at the pump plummet. Of course we wouldn’t buy an SUV, but hearing statements like that makes you wonder what all the talk of peak oil has been about over the years. Right on the heels of that came the Amaranth Advisors collapse. This hedge fund had directed 56 percent of its capital into energy investments and was on the verge of announcing a new energy fund. Amaranth is estimated to have lost US$6 billion, cutting its value by more than half. The company has been mentioned in the same breath as Long Term Capital Management (LTCM), the hedge fund that collapsed at the height of the Russian/Asian crisis. Curiously, that 1998 collapse was also at the bottom of the energy market. Will lightning strike twice? Does the collapse of Amaranth signal not the end of the energy bull, but the start of the next major move up? While we have listened to and read numerous reports of the demise of the “oil bubble” or the “commodities bubble,” it is not surprising to find some who take the opposite view. But first, just what is a market bubble? A market bubble (which may be in stocks, commodities, or even housing) is an economic bubble where we see an exaggerated bull market. The price of stocks, commodities or housing goes beyond all economic sense, rising on a wave of massive public enthusiasm. The earliest introduction we had to bubbles was reading a book entitled Memoirs of Extraordinary Popular Delusions and the Madness of Crowds. The book was written in 1841 but its lessons remain valid today. It covered only three bubbles but each of them was spectacular. They were the Mississippi land scheme of 1719-20, the South Sea Bubble (also around 1720), and Tulipomania in the 17th century (starting in 1634). Over the past few decades we have had a number of bubbles, the most recent being the dot-com episode of the late 1990s. Others have included a biotech bubble in the 1980s and the Japanese stock market of the 1980s. Of course, we also went through the stock market bubble of the 1920s, and in the 1840s in Britain there was a railway bubble. Some say that today’s housing market has become a bubble, and certainly in some cities and regions prices and speculation was reaching a fever pitch. But an oil bubble or a commodities bubble? We don’t think so. And other analysts, including Adam Hamilton in an article dated September 15, 2006 entitled “Oil and XOI Corrections,” also does not believe it. Consider some of the bubbles of the past. Dow Jones Industrials, 1921-29: +482 percent. Tokyo Nikkei Dow, 1982-90: +468 percent. NASDAQ, 1989-2000: +1,365 percent. Oil, 1972-80: +1,233 percent. Gold, 1971-80: +2,328 percent. At the most recent highs, oil was up 613 percent from its lows in 1998. At their most recent tops, gold was up 196 percent and the Commodity Research Bureau (CRB) Index was up only 115 percent. Not what we would call bubble territory yet although oil’s gains could be construed as bubble territory. But bubbles are usually made on almost straight up moves and the chart on the rise of oil prices puts that theory to the test with its jagged rise punctuated by numerous corrections. That is normally a sign of strength not bubble like conditions.

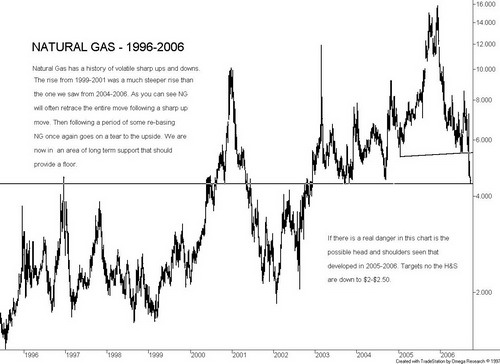

Chart courtesy of www.chartoftheday.com Some considered the rise in Natural Gas prices from a $4.57 low close in 2004 to a high close of $14.31 (actual high was near $15.78) a bubble. But the rise was only 213 percent. The subsequent collapse, though, has retraced almost the entire up move. Natural gas has a track record of rapid rises followed by equally rapid drops often retracing 100 percent of the rise, so this is not unusual in itself. While oil prices are up from their lows of near $11 in 1998, prices in real terms are below the highs seen at the heights of the Iranian crisis in 1979-80. Today, oil would have to rise towards $100 to equal those levels. Further, oil’s importance in the economy is a lot less today then it was in 1979. Note, however, the way that high oil prices have often preceded a recession. We suspect that oil prices would have to sustain a level over $100 per barrel today to generate the same economic problems as we saw in 1979-80. While the public has expressed concern over the high level of energy prices, we have not noted that it is amongst their major concerns. From that perspective oil is not in a bubble, because if it were, the public would be talking about it and nothing else. Adam Hamilton also pointed this out, and he added that he is just not hearing gold stocks, or oil stocks, or penny mining stocks being the constant topics on the cocktail circuit or in the grocery line. Penny mining stocks (which had their own minor bubble in the mid-1990s) have had some nice runs, but with isolated exceptions the gains have been neither spectacular nor sustained. Another measurement of a bubble that Hamilton noted was P/E ratios. At the top of the NASDAQ mania in 2000, P/E ratios were well above 100 and some were over 200. It was clearly not sustainable. The average P/E of the XOI stocks today is 8.5 – hardly manic. A quick check of the Globe & Mail reveals such stalwarts as EnCana (ECA-TSX) with a P/E of 6 and Exxon Mobil (XOM-NY) with a P/E of 10. If anything, they remain cheap. Oil prices are rising for the simple reason that demand is exceeding supply, or at least on the basis that continued rising demand is not being met with new major wells coming on stream. There has not been a major discovery for over 30 years and virtually all major fields, including the renowned Saudi oilfields, are starting the downside of their production reserves. Daily global oil demand is around 84-85 million barrels and is growing each year by 1.5 to 2 million barrels per day. At that rate, by 2020 we could be using over 100 million barrels per day, with the increased demand coming primarily from India and China. We do note that short term supply can at times exceed current demand thus putting temporary downward pressure on oil prices until the equation rebalances itself once again. The obvious question is, if we are reaching peak oil, where are we going to find sufficient oil to meet world demand? The USA alone continues to use roughly 25 percent of daily oil supply, or around 20-21 million barrels per day. Imagine if China used oil like the US did. They would need 80 million barrels a day just for themselves, not the current seven million. Of the 20 million barrels a day the USA uses, only around eight million comes from domestic production. The rest must be imported. There are three arguments going around. One is that the world is running out of conventional oil sources and we are entering the era of falling production. The Mid-East today satisfies roughly 30 percent of global supply. Of more importance, however, the Mid-East has roughly 65 percent of global reserves and some have projected that by 2020 they may hold over 80 percent of global reserves of conventional oil. Of those reserves, Iran and Iraq currently hold about one-third. It is believed, however, that undiscovered oil under the sands of Iraq and in Iran could easily double current reserves there. As well Iran in particular and Iraq hold over 40 percent of the Mid-East’s natural gas reserves, which represents just under 20 percent of global reserves. It underscores the importance of the region to the rest of the world and to the USA in particular. Quite apart from declining production, the obvious trouble with conventional oil is that much of the remaining reserves are in a volatile region of the world where wars and the threat of wars dominate the political landscape. Iran in particular is very important to China’s strategic interests. China is a big importer of both oil and gas and its investment in Iran’s energy sector – already in the $100 billion area – is forecasted to exceed another $100 billion over the next 20 years. The past few years has seen a strengthening of ties on an energy and a military level between China, Russia and Iran. The real target in the current war of words (that may become a real war) between US/Israel and Iran could be the disruption of the ties by Iran to Russia and China. The second argument is that huge reserves of unconventional oil can replace or greatly supplement the world’s oil reserves. GaveKal, a global investment research and management firm that provides numerous financial services globally outlined a number of challenges to conventional oil in a recent article Oil: Will the Malthusian View Carry the Day? – Charles Gave, August 24, 2006. While we do not always agree with GaveKal we do take their points seriously. For unconventional oil, Canada plays an important role with the Alberta tar sands, estimated to hold 178 billion barrels of oil a size that rivals the reserves of Saudi Arabia. There are also the shale fields in the western USA and Venezuela that may hold three to five times the reserves of Saudi Arabia. Finally, the globe still has huge reserves of coal that can be converted to oil. The trouble with all of these sources, however, is that they are expensive to extract, they are dirty (potentially causing incalculable pollution), and extraction is not easy, consuming huge amounts of natural gas and water in the case of the oil sands. Tar sands projects are already causing huge infrastructure and employment strains in Alberta. There are major shortages of technicians. Pollution is becoming an increasing problem with growing incidences of cancer in native populations; there is heavy use of water particularly from the Athabasca River and falling water tables (it is said that it takes 5 barrels of water and enough Natural Gas to heat a home for 4 days to produce a barrel of oil); and, there are growing mutations in the fish population. Current extraction costs are around US$30/bbl but that is just for the easy extractable bitumen. To go deeper may cost more, use even more water and natural gas and cause even more pollution. There is serious talk of using nuclear power to extract the oil, which given the costs to build a nuclear power plant could raise the costs even further. Currently the tar sands produce only one million barrels per day, and even the most optimistic forecasts talk of only four million barrels per day by 2030. So oil from the tar sands to meet growing global demand is limited, despite the huge reserves. Coal, as we noted, is very dirty. As well the cost of moving coal is high when compared to oil. Finally the technology to convert coal to oil and prevent massive pollution seems to be forever in the development stage. There are numerous coal/oil conversion technologies, including some currently in use, but we still do not have the major technological breakthrough. Coal reserves in North America are huge, dwarfing the oil reserves of the Mid-East. Another part of the unconventional oil picture concerns oil/ethanol from agricultural products. The debate here is that it takes more energy to produce a gallon of ethanol than the energy contained in a gallon of ethanol! While efforts are continuing to lower the price, one further problem is that it takes more ethanol-gallons than it does oil-gallons to propel a car a given distance. So while progress is being made, we are more than a few years away from the point where our use of ethanol might reduce demand for oil. The third argument is that we will make great strides in developing electric cars or hybrid cars or fuel cell technology or bio-fuels. These are all viable solutions for the future but the shift to these technologies is, all things considered, moving at a snail’s pace. As well nuclear energy (which could be a substitution, particularly for electricity to charge cars at night) is expensive. It takes a long time to build a new plant and there remains the question of disposal of nuclear waste. Still, China is one country that is moving ahead swiftly on nuclear plant construction. Also we should keep an eye on the development and use of alternative sources of energy and fuel with the military. Military use of alternative fuels and energy would be the leading edge as it has often been military developments that eventually developed into mass consumer use. The internet and the HumVee are just two examples (although the HumVee, a gas guzzling monster that makes SUV’s seem like gentle gas guzzlers is obviously questionable despite its popularity). But oil is all about the now. And oil is an extremely political commodity – probably the most political one in the world. With two-thirds of the world’s oil reserves sitting in the Mid-East and Central Asia, he who controls that can control the destiny of the world. And while we acknowledge that technological developments and changing the way we use energy will eventually lead to a decline in the use of oil in our economy it is all about the now not the future. If oil is to become smaller in our economies why was it so important today for the USA to find it necessary to invade Iraq, holder of some of the largest remaining conventional sources of oil; invade Afghanistan, strategically important for pipelines to be built down from the Caspian Sea region another region with remaining large reserves of conventional oil; and, consider invading or bombing Iran another country with huge conventional oil and gas reserves and major political, energy and military ties to Russia and China two key rivals for US global domination. But it also begs the question whether the expenditure of billions of dollars (and the cost of thousands of lives) to control the region would be better spent on alternative sources of energy that would not only lessen the US’s need for oil, but the world’s as well. If peak oil is driving the current fight to control the globe’s major sources of oil, then, given those alternatives, it is a colossal waste of money and lives. Once we start looking seriously at the alternatives and push hard to develop them, the price of oil will plummet. Oil certainly since the 1970’s has a history of booms and busts and there is no reason to not believe as GaveKal correctly points out that it can not happen again. Here we are in complete agreement. Until that happens, though, peak oil and the continued demand for it will continue to maintain an upward push on global prices. And the real explosion is still to come, when war breaks out between Iran and the West that could encompass the entire globe. Then and only then will we see the bubble that many have said has been burst today.

Charts created using Omega TradeStation. Chart data supplied by Dial Data. David Chapman is a director of Bullion Management Services the manager of the Millennium BullionFund www.bmsinc.ca Note: The opinions, estimates and projections stated are those of David Chapman as of the date hereof and are subject to change without notice. David Chapman, as a registered representative of Union Securities Ltd. makes every effort to ensure that the contents have been compiled or derived from sources believed reliable and contain information and opinions, which are accurate and complete. The information in this report is drawn from sources believed to be reliable, but the accuracy or completeness of the information is not guaranteed, nor in providing it does Union Securities Ltd. assume any responsibility or liability. Estimates and projections contained herein are Union’s own or obtained from our consultants. This report is not to be construed as an offer to sell or the solicitation of an offer to buy any securities and is intended for distribution only in those jurisdictions where Union Securities Ltd. is registered as an advisor or a dealer in securities. This research material is approved by Union Securities (International) Ltd. which is authorized and regulated by the Financial Services Authority for the conduct of investment business in the U.K. The investments or investment services, which are the subject of this research material are not available for private customers as defined by the Financial Services Authority. Union Securities Ltd. is a controlling shareholder of Union Securities (International) Ltd. and the latter acts as an introducing broker to the former. This report is not intended for, nor should it be distributed to, any persons residing in the USA. The inventories of Union Securities Ltd., Union Securities (International) Ltd. their affiliated companies and the holdings of their respective directors and officers and companies with which they are associated have, or may have, a position or holding in, or may affect transactions in the investments concerned, or related investments. Union Securities Ltd. is a member of the Canadian Investment Protection Fund and the Investment Dealers Association of Canada. Union Securities (International) Ltd. is authorized and regulated by the Financial Services Authority of the U.K. |

| Home :: Archives :: Contact |

SATURDAY EDITION July 4th, 2026 © 2026 321energy.com |

|