|

SATURDAY EDITION August 1st, 2026 |

|

Home :: Archives :: Contact |

|

|

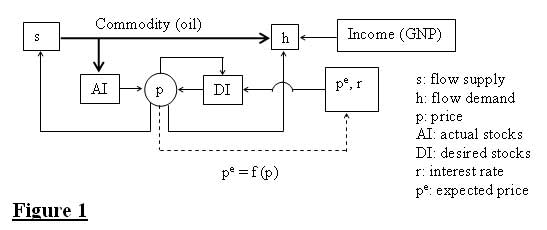

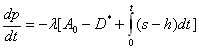

An Almost Friendly Update on World OilFerdinand E. Banks January 08, 2007 Perhaps the best way to begin is to say that I find it difficult to accept that there are still serious students of the oil markets who believe that the crust of the earth is flush with oil, and a global output peak will not take place for many decades, if ever. Other observers aggressively maintain that technology can take the place of natural resources, by which they mean in the short as well as the long run. I mentioned several of these pundits in my energy economics textbooks (2000, 2007), but one escaped my attention. His ‘approach’ will be given some attention below, because recently the prominent U.S. publication ‘Newsweek’ devoted an entire issue to energy matters, and this conspicuous ‘optimist’ provided the first major article in that very ‘special’ issue. I want to make it clear, however, that I am not as concerned with what will happen with oil as I am with what could happen. I know what would happen if I were pressing the buttons and pulling the strings, but for reasons that cannot be gone into here, I would be very surprised if the ‘con’ were placed in my friendly hands. (The ‘con’, as readers or viewers of ‘The Caine Mutiny’ know, generally refers to the command of a navy vessel.) To my way of thinking, the ideal written or spoken discourse on world oil does not avoid theoretical issues, but at the same time is easily absorbed. It attempts to provide anybody and everybody having a genuine interest in the topic with enough information to impress at any hour of the day or night friends, colleagues, and potential employers. An effort would also be made to keep esoteric concepts at a minimum, although when these are essential the presentation remains within the framework of mainstream economic theory. Higher mathematics are not taboo, but would be carefully isolated, because it is – or should be – clear that the learned journals of economics have lost a great deal of their shine due to an excessive reliance on symbolic materials. An example might be useful here. Professor Franklin Fisher of MIT and myself were perhaps the first economists to provide a meaningful discussion of the role of inventories (i.e. stocks) in the pricing of mineral resources, where the initial objects of our attention were tin and copper. Inventories figure in almost all of my work on oil, but occasionally without much enthusiasm, because I have always believed that long-term phenomena were crucial for understanding the oil market. I still consider this to be true, although I have come to recognize that short-term pricing can no longer be discounted. Among other things, I have noticed that global oil inventories often increase without causing a weakening of oil prices. Employing the kind of logic associated with yield curves in financial economics, this might be attributed to an anticipation of supply disruptions. Davies and Nerurkar (2006) have concluded that the oil price is not always determined by what they call ‘fundamentals’, but it was unnecessary for them to propose that the main issue here is an increase in the risk premium. Instead, it is the size of rather than the change in risk premia that is the best explanatory factor for the behaviour of inventory holders. If I believe that the price of oil will reach 200 dollars per barrel (= $200/b) next week, I wouldn’t require an increase in my aversion to risk before commencing to fill my front yard and every room in my house with motor fuel. The pertinent oil consumption and import statistics for 2006 are not yet available, but they will not differ too much from those given in BP’s ‘snapshot’ for 2005. The total global energy use was 2.7% higher than the previous year. About 90% of commercial energy came from fossil fuels (36% oil, 24% gas, 28% coal), with coal the most rapidly growing energy medium: 5% globally in 2005. According to statistics in the tenth edition of Energy Politics, the 5 largest energy users consumed almost 70% of the world’s primary energy, which was an important input for producing 80% of the global GDP. The largest energy users (in descending order) were the U.S., EU, China, Russia, Japan and India. The countries to notice on this list are China, Russia and India, because although their per-capita consumptions are still very low, if present growth trends are maintained, both per-capita and aggregate consumptions will increase by very large amounts in the next 10 years or so – so large in fact that it is highly unlikely that the supply of oil and natural gas can expand to the extent that large price increases can be avoided. (Primary energy is energy obtained from the direct burning of coal, gas, and oil, as well as electricity having a hydro or nuclear origin. By way of contrast, electricity obtained from burning fossil fuels is a secondary energy source.) WHO’S GOT THE (OIL MARKET) ‘CON’? According to Leonardo Maugeri, the people who have it now are identical to those who enjoyed its possession before the first ‘oil price shock’, or for that matter most of the years after that traumatic episode. By that he means consumers, firms and governments in the major oil importing countries. The editors of Newsweek almost certainly share this opinion, because otherwise Maugeri’s contribution would have been relegated to a less conspicuous position in their magazine, regardless of the fact that Signor Maugeri is an officer of ENI – which not only is one of the largest corporations in Italy, but for many years has been a noteworthy international player in oil, gas, electricity, petrochemicals, etc. He is also the author of a book about oil called ‘The Age of Mythology’, which on select occasions I have described as a half-baked, unscientific song-and-dance designed to expose the ignorance of persons like myself in the matter of “the world’s most controversial resource”. ‘Game Theory’ has become a very important subject in academic economics, however not as important as I thought it was when I taught it many years ago. For instance, Professor Erich Röpke was far from being completely wrong when he called it ‘Viennese coffee house gossip’. As Chris Skrebowski (editor of The Petroleum Review, a monthly review published by the Energy Institute in London) has indicated, there are so many untruths and misunderstandings where oil is concerned that it is almost impossible to carry out a straightforward economic analysis, however the systematic use of deceit and deception is what an appreciable part of game theory – or ‘interactive decision theory’ – is all about. (A number of valuable insights into this topic can be gained from perusing an elementary textbook such as Dixit and Skeath (2004). The fabrications alluded to by Skrebowski, and launched by many self-appointed oil experts, are often intended for consumption by the major oil producing countries, particularly those in the Middle East. Their ulterior purpose is to convince the governments of those countries that if they do not ‘open’ their economies to direct or indirect foreign influence, they are riding for a fall. Of late this crank contention has also been forwarded to some important movers-and-shakers in Russia, although it needs to be emphasized that while President Putin openly disregards this foolishness, the governments of the Middle Eastern countries have skillfully managed to conceal their disdain for the advice, disinformation and bizarre claims of Signor Maugeri and his admirers. I can also reveal that the ENI stronghold in Milan is well known to this humble teacher of economics and finance, since I have attended conferences there and lectured at the ENI Corporate University, but even so I have never encountered a single ENI employee of any rank, in that city or anywhere else on the face of this good earth, with the same twisted vision of world oil as the one that Maugeri posted in Newsweek. I feel it necessary to confess though that in the light of my long and intensive study of energy economics, it would hardly make any difference to me if the testimonials of Mr Maugeri’s supporters – if he has any – were accorded the status of holy writ. As I make clear in an early chapter of my new textbook, the large oil producers have the oil market ‘con’, and are in position to make the most of it. Whether they will do so or not is quite another matter, and if they do the likelihood of it conflicting with the energy requirements of the major oil importing countries, and how, cannot be examined in this brief discussion. First and foremost it needs to be recognized that our political masters would do almost all of us a favour if they took the liberty of ignoring the greater part of what Signor Maugeri and Newsweek’s in-house experts have to offer. Consider the following. Maugeri states that the average global recovery rate for oil 30 years ago was 20%, when actually it was 32%, as compared to 35% at the present time. The purpose of this spurious comparison is to convince readers that improvements in recovery technology are accelerating, when the opposite is probably true. He is also attracted to the “dim but intriguing prospect” that oil might be a “renewable resource”. To clarify this ludicrous prospect the editors of Newsweek called on the Harvard chemist and Nobel laureate Dudley Hershback. Unfortunately however their interviewer asked Professor Hershback one question too many. When pointedly requested to comment on whether it was possible to significantly increase oil reserves or to endlessly regenerate oilfields in accord with the looney-tune logic developed by Thomas Gold (1999). Hershback’s answer – while appropriately flippant – was more suited to the type of offbeat rambling that might be found in a store-front university than in the seminar rooms of an Ivy League institution of higher learning. “It may be that you have to go to pressures and temperatures 500 miles down in the Earth, and there’s no prospect of drilling. It may take 1000 years to percolate to the surface. I would not be surprised if that’s the actual outcome. It would be charming if, after our generation has burned up all the oil, 1000 years from now our successors, if there are any, say ’Gee, all of a sudden we have all this petroleum again. Now we can have cars again. It’s nice that there are a few left in the museums.’ But if that’s the case it’s not a practical use for humanity in the foreseeable future.” 500 miles down into the earth, and 1000 years to “percolate to the surface”. This sort of thing is reminiscent of the “miracle weapons” that Adolf Hitler promised the German people toward the end of WW2 in order to convince them to continue accepting the devastating punishment that was being inflicted on Germany by the U.S. and UK air forces and the Russian army, except that even at the most flamboyant and irrational stage of his career, Der Führer would hardly have dared to request the faithful to wait a full millennium for their dreams to come true. Experts and pseudo-experts provided about half of the articles in this special edition of Newsweek. The remainder originated with ‘regular’ columnists in that periodical, as well as some individuals whose position in the scheme of things is difficult to describe. As an example of this remainder, the submission of the Newsweek columnist Fareed Zakaria features what is known in Sweden as a ‘nid-bild’, which is a caricature designed to show the most unfavourable aspects of a subject’s physiognomy. The persons in this cartoon are the presidents of Iran, Russia and Venezuela. Mr Zakaria is greatly annoyed by the flouting by Iran, Saudia Arabia, Russia and Venzuela of what he calls “rules” Exactly what rules are these? They are stipulations fashioned outside these countries that are designed to make fools of gentlemen like those shown in the aforementioned cartoon, their constituents, and especially millions or hundreds of millions of persons on the buy side of the oil market who might be gullible enough to believe that the presence of a few corporate jet setters on the sidewalks of Teheran or Moscow will make the nonsensical energy forecasts of Mr Maugeri come true. Although there are a few exceptions, the dialectics of mainstream economics is as remote to many Newsweek employees (and stringers) as that of quantum physics. Zakaria apparently believes that the governments of the OPEC countries and Russia should have the decency to invest their oil windfalls in expanding production and exports, but the time when such departures could be regarded as part of a sensible agenda by the owners of these assets is probably past. The fundamental message that needs to be considered here is as follows. The rich invariably have more options than the poor, and as a result of the oil price increases that began about two years ago, many of the oil exporters are no longer afflicted with an uncontrollable compulsion to play Father Christmas for the motorists of the oil importing world. Saudi Arabia, for instance, may have recorded a surplus in excess of 70 billion dollars for 2006, which should make it possible to increase foreign assets by a very large amount, while at the same time greatly reducing public debt. Equally as significant, that country and others have finally come to appreciate that resource nationalism isn’t just a good thing – it’s the only thing for those who have the means to practice it! This is one of those golden rules that I learned and later taught at IDEP – i.e. the African Institute for Economic and Development planning in Dakar, Senegal. (IDEP) – where I spent a large part of my time examining the brilliant work of the late Harvard economist Howard Chenery. Unfortunately the mathematics used by Chenery, together with my general disbelief in the leadership and curriculum of that establishment, were strongly unappreciated by many colleagues and a few students, however it soon became clear to me and most of the others that resource nationalism may make a great deal of sense as a means for initiating sustainable growth. Having gone that far, it might be appropriate to proffer an optimal strategy for the governments of the main oil importing countries. There has been an extensive discussion about replacing oil imports by environmentally ‘friendly’ fuels such as ethanol and hydrogen. If this were done the right way, it might help everyone, because as pointed out on a number of occasions in both articles and comments in the important energy forum EnergyPulse (www.energyforum.net), exports of oil and gas are of crucial importance for many energy exporters, even if the increase in their wealth over the past few years means that they are no longer under the same pressures to expand their supply as earlier. The point then is to make sure that there is always sufficient production capacity for alternative resources available to the oil importing countries to dampen undesirable and potentially hazardous oil price escalations. In the long run this capacity conceivably makes more sense than trying to contain oil price escalation with inventories, which is apparently a belief of the present U.S. Energy Secretary. According to Björn Lindahl (2006), that gentleman also wants China (and presumably a few others) to place more reliance on the international oil market than initiating or joining a frenzied bidding for equity positions in certain oil producing countries. I would be very surprised indeed if a country like China was willing to base a significant portion of its energy future on the possible uncovering of bonanzas in Central Africa or, for that matter, on the established petroleum exchanges in New York and London, although in the short run these options might be attractive. The expression ‘workshop of the world’ that one hears these days must sound divine to the ears of the Chinese leadership, and they realize that adequate energy in all forms is necessary to perpetuate this characterization. Apparently China has granted about 3 billion dollars in credits and oil-backed loans to Angola, but since the World Bank believes that Angolan output will peak in 2011, and begin to decline in 2012, some question might be put as to how realistic their expectations are. The OPEC countries have recently declared their willingness to defend a price of $60/b, however there is undoubtedly an opinion in some quarters in OPEC as well as some of the oil importing countries, that even in the near future a price of $70/b is both inevitable and tolerable. I don’t recommend accepting this opinion at the present time, and feel that it was a wonderful thing that the price of oil retreated to $60/b before the international macroeconomy was put to the test. The thing to remember here is that if the sustained/equilibrium price was $70/b, price spikes could exceed 80 dollars. This is something that nobody in their right mind wants to have any part of. Exactly how the capacity mentioned about should be accumulated or deployed cannot be discussed in this brief paper, although I am sure that many readers have a few ideas on this subject. If so, these ideas or suggestions should be forwarded as soon as possible to the proper authorities, because there are many observers of the world oil economy who feel that the present optimism about the oil price is unjustified. OLD QUESTIONS ABOUT OIL, BUT A FEW NEW ANSWERS A sharp and alert fly on the wall in the Newsweek editorial offices would have discovered at an early stage of the discussions about the above noted energy ‘project’ (labelled “Breaking Out”) that the editors of that publication were engaged in slightly more than impartial reporting. Their special issue was produced in cooperation with the World Economic Forum, which is an annual conclave of well-dressed movers-and-shakers from the exclusive turf of money and influence. To ensure that their eulogies to globalism and technology are given the widest possible publicity and/or dissemination, that elegant talk-shop is held in the marvellous Swiss skiing resort of Davos. To keep up appearances, Newsweek allowed Matthew Simmons – author of Twilight in the Desert: The Coming Saudi Oil Shock and the World Economy – to present a fragment of the oil pessimists argument. Equally as interesting was the contribution of Bruce Sterling, who emphasized that oil is an input for everything from “hair gel to home appliances”, but that could change if the price of oil escalates. In his opinion, this change would not be something to look forward to, and would carry an odor of “mild decay”. I presume that he is talking of economic decay, which in turn could lead to the kind of unappetizing scenarios that feature painful and extensive political, sociological and cultural disruptions. The Nobel Laureate Sir Harry Kroto once mentioned this sort of thing while discussing what an oil price escalation would mean for the price of fertilizers. This is a topic that has not received the attention that it deserves, although the former Shah of Iran was arguably correct in insisting that oil was too valuable to be used primarily as a motor fuel, by which he meant that a too rapid exhaustion of oil reserves would eventually be very bad news for the consumers of petrochemicals – who happen to be all of us, whether we dress our hair with Brylcream or axel grease. In my lectures and books I never miss an opportunity to point out that regardless of the amount of money being spent on exploration and production, and regardless of the advances of technology, each decade sees a sharp decrease in the discovery of reserves. Simmons indicates that the last super-giant oil field discovered was the Cantarell Field in the shallow waters of the Gulf of Mexico, in l976. He did not bother to mention though that that field has already peaked, and its production will comparatively soon be approaching one-half of its maximum output. We can encounter disturbing phenomena of this nature everywhere. Oil production in the U.S. peaked in late 1970, but later the huge Prudhoe field in Alaska came on stream. The declining production curve then turned up, however well before it reached the previous peak it turned down again, following which the import of oil by the U.S. escalated. This peaking of individual fields is something that was studiously ignored in the Newsweek presentation, but it happens to be of vital importance for almost all of their readers, to include those who prefer Frank Sinatra to Daddy Romance. 70 percent of the world’s oil production reputedly takes place in fields with a falling output. A year ago Chris Skrebowski said that 18 large oil producing countries, and 32 smaller ones have falling production, and they will be joined by Denmark, Malaysia, Brunei, China, Mexico and India soon. Note that in the case of e.g. China and India, although output may still be increasing, imports of oil are already increasing by ever larger amounts. Something to be noticed here is what I call ‘Campbell’s Proposition’, by whom I am referring to the well-known Irish petroleum geologist Colin Campbell. He says that for a given region, production curves for oil will approximately resemble discovery curves. This is definitely not good news. U.S. oil discovery peaked in l930, and production in l970-71. Discovery peaked in the UK North Sea about l975, and output close to the end of the 20th century. The global discovery peak for conventional oil was 1965, which has made some observers claim that a global output peak could come at any time. I don’t believe this because I suspect that some large oil importers are prepared to use their military assets to prevent this from happening., however it seems useful to record that the very competent analysts at Deutsche Bank have predicted that the global peak will come in 2014. To witness oil fields in every part of the world peaking, but yet to claim that there will never be a global peak, requires an explanation completely divorced from conventional logic. China was self sufficient in l993, but in the following year imported 135 million tonnes of oil. Norway has been a major exporter of oil for the last decade, and has always done its part to prevent the oil importing world from being discomforted. Their oil output recently peaked, and since discovery in their part of the North Sea peaked many years ago, nobody really believes that they will be able to live up to the occasional bombastic claims about large new finds. An impressive new discovery was made in India several years ago, but even so domestic supply is only about 25 percent of requirements in that rapidly growing country. Perhaps the most important reference for this discussion is the Oil and Gas Journal. Its editors do not believe that the oil peak can be delayed past 2020, and will likely come sooner. In addition, according to the important consulting firm HIS Energy, there are few if any major discoveries still to be made. The other side of the story is presented by the Cambridge Energy Research Associates (CERA) in Boston. It goes like this: large increases in the oil price would precede or coincide with a peaking of production. This would encourage efficiency, substitution, and conservation. New oil discoveries would take place and there would be added emphasis on investments in alternatives to oil. Accordingly, those gentlemen believe that the concept of a peak is misleading. As far as they are concerned we will witness an undulating plateau. A few influential students of the oil market say that this picture is correct, while a large majority say that it is wrong. In reality it doesn’t make any difference, even if it is more wrong than right. Undulating means that a global peak will arrive, followed eventually by recovery, and at some point after that there will be another peak, followed by…. The problem is that in the valleys after the peaks, the international macroeconomy could suffer convulsions on the order of those experienced during the great depression (1929-1936). I also think it necessary to suggest that this pseudo-scientific concept of an undulating peak is the kind of thing that turns up late at night in working dinners or client ‘encounters’ that feature a heavy consumption of expensive alcoholic beverages. When could this peak arrive? Somewhere around one trillion barrels of oil have been extracted so far in human history, and Campbell believes that another trillion will become available sooner or later in known fields or fields in the yet-to-find category. Numbers like these have led a French government analysis to predict a global peak in 2013 or thereabouts. The oil ‘major’ Chevron also seems inclined to use these figures in their advertisements. They say that while it took us 125 years to use the first trillion barrels of oil, it will take us just 30 years to use the next trillion. As I explain in my new textbook, it might actually take us several thousand, although it hardly makes a difference, because these numbers immediately suggest that it might be very difficult to delay the global peak for oil past 2020. I can also mention that whatever the peak output turns out to be, it will involve both conventional and unconventional oil . As indicated by Aguilera in his informative PhD Dissertation (2006), all varieties of unconventional oil are steadily receiving more attention, but unlike several of Dr Aguilera’s ‘references’ (e.g. Sir Alan Greenspan and Michael Lynch), the belief here is that in the near future liquids from tar sands, coal and gas, heavy oil, etc have much less to offer than commonly believed, and under no circumstances will be available at the bargain basement prices occasionally advertised. For example, Venezuela contains a huge amount of reserves in the Orinoco ‘heavy oil belt’, and given his various ambitions and the cash flow at his disposal from conventional reserves, there is little doubt that Major Chavez would spare no effort to exploit these reserves if the cost were not excessive – which it is. Something else to remember is that enough oil must be produced every year to provide for both the rate of growth of consumption and the (little understood) natural decline rate. Campbell prefers an ultimate reserve estimate of 2 trillion, but there are organizations which believe that this figure should be 3 trillion, with well over a trillion consisting of ‘hypothetical’ discoveries. My opinion is that regardless of the truth, 3 trillion is not a healthy estimate to work with or bandy about at the present time, because it fosters an unhealthy optimism. An interesting point here is that while many observers claim to be able to judge the extent of discoveries that have not been made, they are not completely certain about the composition of those which were verified years ago. A good example is the giant Kazakh oilfield, which according to some commentators is set to smash forecasts, and whose exploitation involves such big names as Total, Royal Dutch Shell, ExxonMobil and Conoco-Phillips, as well as a few smaller enterprises who have judged the prospect a worthwhile investment. Whether we are dealing with dubious forecasts or hype is very uncertain, because Kashagan has sometimes been labelled the most complicated field in the world, and only a few years ago it was suggested that its prospects were highly overrated. One thing is certain: given the likelihood that it will be an enormously expensive project, and given the bad odour into which some of the directors of big oil have fallen, it is easier to deal in over-optimistic and/or mendacious claims than to stick to the truth. Just as important, even if Kashagan lives up to its billing, it and all the other fields in the Caspian cannot pull the center of gravity of global oil production away from the Middle East, as some observers have mistakenly chosen to believe. The IEA has announced that 120 mb/d of oil will be produced in 2030, while the CEO of the French oil major Total insists that 120 mb/d will never be produced. The latter sounds right on the money to me, if only because Saudi Arabia will never produce the 20 mb/d that are implicit in the IEA’s estimate. Kenneth Rogoff, a Harvard Professor and the former chief economist of the IMF, thinks that speculation about peak oil is a waste of time. In The Economist (April 22, 2006) he says that “the oil market is highly developed, with worldwide trading and long-dated futures going out five to seven years. As oil production slows, prices will rise up and down the futures curve, stimulating new technology and conservation”. Where futures are concerned his numbers are right, but the units are wrong. The correct maximum is 5 to 7 months. Beyond that Rogoff should be made aware that liquidity is completely inadequate, and there have been periods when liquidity was insufficient beyond 3 months. Unfortunately this is not the place to launch a discussion of substitutes (in one sense or another) for oil, nor am I particularly qualified. I cannot help believing though that Governor Schwartzenegger of California has the right idea, although many very knowledgeable participants in the forum EnergyPulse question his partiality for biofuels and hydrogen, etc, since these have been the object of some intensive debunking exercises by a number of highly qualified researchers. Even so, I cannot submerge my belief that – on the basis of information coming my way over the past few years – it makes more sense to place a modest bet on these assets than oil from tar sands, heavy oil, and very definitely shale. Needless to say, I could be very wrong here, however I expect this matter to be given a thorough investigation in the next few years, since most of the decision makers have decided to recognize that a new departure is appropriate where motor fuel and environmental matters are concerned. A STOCK-FLOW MODEL OF THE SHORT-RUN PRICING OF OIL Some of the background for the following discussion can be found in recent issues of the (London) Financial Times, where there is a short discussion or mention of the oil price at least several times a week, and generally with a reference to inventories. About the diagram below. I have used this is many of my courses in economics, and all my courses in international finance, where I carefully explained to my students that if they fail to understand its simple mechanism, they are almost certain to receive a failing grade. The problem elsewhere, and particularly in my articles, is that readers do not realize how simple this diagram is. What will be done here is to begin by making clear that we have a simple stock-flow arrangement, where what is known in economics as equilibrium is attained when existing inventories are equal to desired inventories. This is commonly called a stock equilibrium. What about the flow supply and demand curves that you were introduced to in your first course in economics? It turns out that when flow demand is not equal to flow supply, these inventories are changing. This is a very uncomplicated process, and it will be explained to some extent before a small amount of serious mathematics appears. The important observation here is that the stock equilibrium takes precedence over the flow equilibrium, and given a stock equilibrium we have a flow equilibrium – but not the opposite. In any event, readers of this paper can and should review the discussion below until they arrive at the mathematics! At that point they can decide whether to examine the equations that are presented, or go directly to the conclusions. One more thing. The diagram below is not intrinsically related to those interesting diagrams that you encountered in your electrical engineering textbooks , although there is a passing resemblance. This is because the ‘circuit’ containing p and DI is equivalent to what is known in electrical engineering as a first-order servomechanism. No big deal will be made of this observation in the present discussion, however if readers become interested enough to solve and examine the differential equation that will be formed later, this property has much to do with the presence of unstable outcomes. Let’s also notice the following: s, h, DI, and AI are physical items, while e.g. ‘p’ and GNP are financial items. In looking at the physical circuit we need to understand that just as oil can move into inventory, as shown on the diagram, it can also flow in the other direction. The reader might want to add another arrow to indicate this. Note also that while DI is labelled a physical item, this is because of its units – which as in the case of AI are barrels. There are no barrels of oil going into DI as there are in AI, but inventory holders might wake up one morning with a belief that oil prices will increase (i.e. pe ↑) because of e.g. recent (correct or incorrect) information they received about the movement of future prices, and so they want larger inventories. In the mathematics below no complicated behavioural equations will be formulated for inventory holders for the simple reason that the result would deserve the classification of pseudo-scientific. Note that DI is influenced by both price and expected price. If a decision was reached to increase inventories of oil, and in doing so the oil price increased by a large amount, a decision might then be made to reduce the speed at which inventories were being increased – depending on the pattern of expectations. There are many possible scripts that can be written for this drama. Something that needs to be appreciated is that a diagram such as Figure 1 is most useful when used to describe price formation in the global oil market, even though it would be very difficult to develop an expression describing the formation of a ‘global’ expected price (pe). I don’t worry about that any more however. What I want is for my students to be able to understand that when AI ≠ DI, inventories will change. If, for example, DI > AI, then present (i.e. flow) production must exceed present (flow) consumption in order to permit oil produced during a given period to move into inventories. How do we get this? Well, as in the first course in economics, beginning with an equilibrium (DI = AI), the oil price must increase: this raises flow production (s) and reduces flow consumption (h). The difference between the two is the amount, per period, going into inventories.

Even in elementary mathematical economics textbooks such as Chiang and Wainwright (2006), the discussion above suggests the formulation of an equation in which the change of price with respect to time is a function of the difference between AI and DI. In the future these will be designated A and D, and at this point we can remember some advice of Professor Lipman Bers (1975), which is that whenever possible we should be on the hunt for differential equations. The relevant equation might be dp/dt = f(D – A). Let’s write this in the following explicit way: dp/dt = λ (A D) . The following expression should be self explanatory if we take for the flow values s = s(p) and h = h(p), A0 as the initial value of actual stocks, and D* the desired inventories.

A differentiation of (1) with respect to ‘t’ will then immediately yield: d2p/dt2 = – λ[ s(p) – h(p)] (2) What about a solution for this simple differential equation? My answer on the present occasion is to compare it with the differential equations we might encounter in ballistics – for instance those for the trajectory of mortars and recoilless rifles. These relationships are well known to students of analytic geometry, and have been well confirmed experimentally. They also provided the basis for some very useful range tables for myself and colleagues at Camp Gifu (Japan), Fort Lewis (Washington State) and Hardt Kaserne (Swaebisch Gmuend, Germany), a few centuries ago. In my present academic work I invariably take linear equations for s(p) and h(p) – e.g. s = α + ap and h = β + bp. These are of course approximations, and perhaps not very good approximations. In addition, λ has to do with the ‘speed’ with which the (s – h) ‘gap’ is closed, and in no circumstances could any numerical value that we assigned be more than an approximation. What we are heading for here is a question as to the optimal extent of this exercise, and probably the correct answer is formulating equation (1) and understanding the logic behind it. As for (2), there might be some small utility in solving this comparative simple second order differential equation and showing how the values of the parameters (i.e. a, b, λ, α, β) determine the stability of the price. CONCLUSIONS AND EXTENSIONS As I unexpectedly discovered when I was circulating a few chapters of my new textbook, certain people deeply resent my making statements such as “oil is scarce” and “the main oil producing countries do not require the ‘hands-on’ assistance of Big Oil”. The simple truth of the matter is that these countries have discovered this by themselves, and for the most part my advice is neither solicited, needed nor appreciated. Moreover, they are not interested in the opposite point of view, although they know enough game theory (or possess enough ‘street smarts’) to give the impression that they are attentive. A useful inclusion in the Newsweek issue frequently mentioned above is a short comment by U.S. Energy Secretary Samuel Bodman. It is highly interesting that at no point did he refer to oil. My deduction here is that since Mr Bodman is very likely on a first name basis with the gentlemen in the executive suites of Big Oil, he would consider it impolitic to convey their privately expressed opinions of the world oil market to the TV audience or the readers of news magazines, which almost certainly do not resemble those that the Newsweek big-wigs are trying to foist on their clientele. One thing however is certain: at virtually no point in modern times has Big Oil been able to revel in the kind of profits that they are realizing at the present time, nor expect to receive, and they are in no hurry to terminate this delightful situation by going on expensive hunts for oil which they believe does not exist – nor for that matter oil which they believe they could find it they looked hard enough. In December, 2006, the Chinese government invited four of the largest oil consuming countries to Beijing to discuss the future of oil. These countries and their consumption (in percent of the global output of 85 mb/d) were the U.S. (24.7%), Japan (6.0%), India (3.1%) and South Korea (2.5%). China’s percentage consumption is 8.6 percent of that output. It was remarkable that Russia was not on the guest list, because one of the points emphasized in my new textbook is that if Russia continues to develop at the present rate, and in particular if the number of vehicles in that country continues to increase at the rate now experienced, their domestic consumption of oil will ensure that the revenues of all oil exporters will not be threatened by such things as the increase in the production of biofuels now taking place in many parts of the world, or even a sharp economic downturn in the U.S. and the EU, because regardless of changes in the global macroeconomy, Russian oil exports are more likely to stagnate rather than expand. The United States Energy Information Agency (EIA) recently offered a forecast of the real (i.e. inflation adjusted) oil price in 2030 of $59/b. Employing an inflation rate of 2%, this implies a nominal (i.e. money) price of oil of $95/b. In Hollywood a film about economists being asked to determine the oil price in 2030 would be called Mission Impossible, although I’m not sure that this title would be accepted by my former colleagues at the University of Stockholm, because those ladies and gentlemen probably know only slightly more about the oil market than full-time rappers and meringue dancers in the less distinguished studios of the film capital. The EIA has also decided that the real oil price will fall until 2015, after which it will increase. Readers of this article are strongly advised not to take these forecasts seriously, because neither the EIA nor anyone else is in possession of statistical or other methods which would permit the generation of usable forecasts over more than a limited time horizon. These forecasts may well be elements of the great oil market game, although I have not given any serious thought to the identity nor the rationality of all the participants. This might be the place to mention that according to the Oil Depletion Analysis Centre (ODAC), which is one of the most important sources of up-to-date information on oil and gas, the UK Treasury has announced that UK oil output will decline by 3 percent a year until 2011. But according to ODAC it was falling by 10 percent a year between 2002 and 2005, and this figure will probably be valid for 2006. The question must then be asked as to whether the downturn indicated by the Treasury is feasible, and if it should take place, would it be durable. My conclusion is that somebody in London or elsewhere has either lost their compass, or decided that it is best for oil consumers in the major importing countries if they ignore the economic, political and geological realities behind the present oil price, and elect to believe that at some point in the not too distant future they will not only have all the oil to which they believe they are entitled, but that it will be available at modest prices. Finally, I would like to point out that my previous energy economics textbook (2000) did not receive the all-inclusive appreciation that I expected. To my great surprise a negative review was fabricated by the book review editor of the Energy Journal, Professor Richard Gordon. Eventually I concluded that one of the reasons for his pique was that I never – and I mean never – miss an opportunity to reveal that in faculties of economics in virtually every part of the world, both teachers and students of resource economics are being forced, or forcing themselves, to confront the bizarre and utterly hopeless model of Harold Hotelling (1931). Please let me assure you that Professor Hotelling was a brilliant economist, even if he did the great world of theoretical economics a disservice by producing that article. I reveal this because on the occasion of a lecture that I gave in wonderful Copenhagen, I was told that even if Hotelling’s model is without an iota of scientific relevance, it must still be taught because of the purported absence of a suitable alternative. Do yourself a favour and try to avoid being on the receiving end of that so-called ‘teaching’. Ferdinand E. Banks ReferencesAguilera, Roberto F. (2007). ‘Assessing the long run availability of global fossil energy |

| Home :: Archives :: Contact |

SATURDAY EDITION August 1st, 2026 © 2026 321energy.com |

|

(1)

(1)