|

THURSDAY EDITION July 9th, 2026 |

|

Home :: Archives :: Contact |

|

|

Ethanol: Is it Viableby Salman Anwar KWR International July 29th, 2006 Summary:

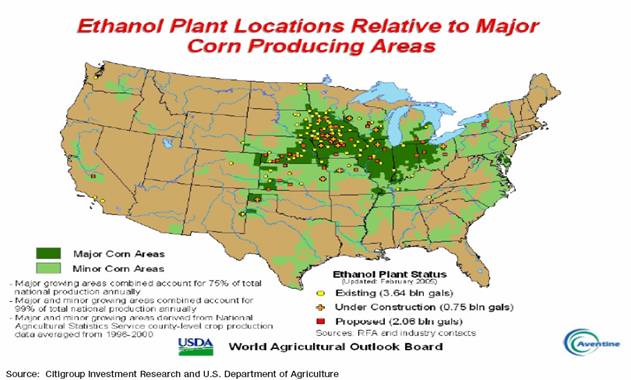

Why Ethanol?The economics behind ethanol do not necessarily demonstrate feasibility. Simply stated, it is unclear whether ethanol will be the solution to U.S. energy woes. At the same time there is currently an inadequate supply of ethanol to fulfill demand. The pressure from government has forced the U.S. to produce 4 billion gallons of ethanol in 2006, with a forecast to increase to 7.5 billion gallons in 2012. This is helping to fuel an ethanol boom that will double the size of the industry by 2008. A number of states have a mandate in place to use 10 percent ethanol as the blending agent, replacing MTBE, which contributes to more environmental pollution than ethanol. An example of that would be Hawaii. As of April 2nd 2006, at least 85 percent of Hawaii’s gasoline must be E10, i.e. 10 percent ethanol. The reason why ethanol can replace MTBE is because they both can serve as blending agents. In the United States, ethanol has been used in vehicle fuel for many years, but only as a blending agent. The recent increase in oil prices and the angst of depleting oil reserves has led everyone’s attention toward ethanol production. Overtime it is likely that Ethanol will become much more important as a fuel source, but the technologies to make that happen appear to be decades away. It took decades for oil to be the main source of energy and years to make it burn more efficiently. The transition in its uses can be seen. For example, first oil was used as medicine, then a lighting fuel, then slowly moving toward its use as an automotive fuel, jet fuel e.t.c. It took time for oil to go mainstream as the main fuel source. The same time factor applies to ethanol; it will take years before ethanol can fully replace oil because basically everything runs on gasoline. For example, the median age of light vehicles in the U.S. vehicle fleet is about 14 years, and it could take about 14 years for the U.S. fleet to be replaced by vehicles that can run on both gasoline and ethanol.  Who’s pushing ethanol?There is an important political dimension to the use of ethanol in the United States. The U.S. farm lobby is strong and promotes ethanol as the fuel of the future especially as it represents considerable profit potential. According to the Organization for Economic Co-operation and Development (OECD), it would require almost a one-third of U.S. farmland, to power one in 10 of America’s cars with homegrown corn–based ethanol*. Consequently, the government is investing in a technology that is not up to the challenge due to land use issues, a weakness in transportation and refining infrastructure, and a very political regime pertaining to keeping potential external sources of ethanol fuel-stock out of the market. According to an editorial The Post-Journal, (Jamestown, New York):“It should come as no surprise that ethanol’s best friends are in farm states — including members of Congress who represent them. Regardless of whether expanded use of ethanol would be good for U.S. motorists, it would help those states.” The study conducted by Alexander Farrell of the University of California, Berkley, published in the Science magazine indicated that corn-based ethanol cuts overall greenhouse gas emissions by only 13 percent compared with petrol. In Brussels, the European Union Commission has found that that the standard production methods for sugar-beet ethanol in Europe reduced global warming emissions by one third. Consequently, the question must be raised as to why we in the U.S. are investing so many resources in corn-based ethanol that reduces emissions by only 13 percent, when it can invest the same resources towards producing sugar-beet based ethanol that reduces the emissions by 20 percent more? The answer, of course, is that it is all about keeping the farmers happy and showing the American public that we are striving towards an independence from foreign oil imports. Who Benefits?Analysts are predicting that by 2008, ethanol production is expected to reach 8 billion gallons, but there remains a scare that the corn demand, could strain food supplies, raise costs in the livestock industry, and ultimately lead to a land rush. Already Agriculture Department economists expect the value of this year's corn crop to climb roughly 20 percent over last year, also elevating the prices of sugar to record levels. The agriculture industry will benefit the most. Companies like Archer Daniels Midland, Cargill Inc., Monsanto, and DuPont that are involved the production of ethanol, corn seed or genetically engineering them to provide the most acreage. There is no disagreement on the issue that the ethanol frenzy will lead to a clean, green alternative to oil and relieve the U.S. from the dependence on OPEC for oil, but many believe it makes more economic sense to import this fuel from Brazil or any other country that produces ethanol more cheaply than the U.S. or is much better than the U.S. in the production method of ethanol. The U.S. therefore would benefit from being less stringent about its policy on ethanol imports, otherwise it will waste its scarce resources in the production of a fuel that is not produced efficiently at an optimal cost. This would require the U.S. to work side by side, and t0welcome the transfer the ethanol technology from, countries that have a competitive advantage in ethanol production. Scrutiny by the U.S. Congress is needed to research more about the expanded use ethanol, before a policy is made to encourage it as the mainstream fuel. Obstacles faced by ethanol: The most significant non-political obstacle the ethanol industry faces in the U.S. is a lack of infrastructure. Unlike oil and natural gas, ethanol or gasoline containing ethanol cannot be transported by pipeline. The current oil refineries cannot be used for ethanol and will need to be converted. The only viable ways of transporting this fuel is either through trucks or waterborne. This is due to the fact that ethanol is soluble in water and thus can be easily diluted and/or contaminated. To develop the infrastructure that supports ethanol, it will require time as well as the investment of resources. Another challenge facing the ethanol business is that most of the ethanol plants are located in the Midwestern United States. Transporting ethanol to the energy hungry East coast and West coast is a daunting task. One helpful factor is that, the majority of the existing and proposed ethanol plants are located on or a near a major waterway, but one thing again poses as a barrier. To equip all the ethanol plants, so they can transport the fuel via water i.e. trucks needed to bring the fuel form the site to the vessel. This is capital and time intensive. Another mode of transport for ethanol is via railroad, but this will require special cars that can transport ethanol. In addition, ethanol would have to compete for limited rail transport space with coal.

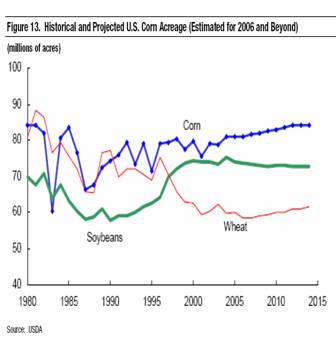

Ethanol economics: Currently, U.S. ethanol production cannot meet demand and imported ethanol is required to balance supply and demand. For the import of ethanol to be economically feasible, it is important for ethanol prices to be above $2.45/gal. That is because if the value of imported ethanol is $1.75/gal and with custom duty and transportation costs of $0.15/gal it is viable subjected to the above quoted price. Currently U.S. ethanol makers can break even at an oil price of $55 a barrel. In the beginning ethanol production will be expensive due to the technology being further researched and developed. In the years to come, there are chances of this technology to take off, but at a cost. For all the challenges facing the U.S. ethanol industry, efforts are being made to meet rising demand. Over the next twelve months, at least 39 new ethanol plants are expected to be completed. The new plants will add 1.4 billion gallons a year to the current 4.6 billion gallons production. This will put the United States ahead of Brazil. But there remains the very basic problem of not having enough cars available for the use of ethanol. Ford, Daimler Chrysler, and General Motors have a flex-fuel vehicles program and the line up is expected to be unveiled by the end of 2006. U.S. Corn Acreage on the rise

A look at Brazil: Similar to the United States, the Brazilian government had also subsidized the production of Ethanol back in the 1970’s. There was also a lot of investment from the private sector into the ethanol industry to make Brazil independent from foreign oil. Brazil is the world leader in flex-fuel cars, and even the Brazilian President Luiz Inacio Lula da Silva has embraced the concept of being independent for energy. Brazil has perfected this technology of flex-fuel vehicles to the point, that for a Brazilian the cheapest fuel choice is clearly ethanol. That is because Brazil produces ethanol so efficiently and cost effectively. Brazilian ethanol is sugarcane-based unlike the corn-based version in the U.S., which requires more time and money. The Brazilian auto fleet is comprised of 20 percent flex fuel vehicles and Brazil is the second largest producer of ethanol. The country has taken to heart an approach of a vehicle that can run on multiple fuels. It has advanced in that aspect to an extent that it hopes to export flex-fuel cars and technology around the world. The idea for non-gas powered vehicles goes back to the 1970’s fuel crises in Brazil, when its economy nose-dived and that is when this initiative was launched. The fruit of that initiative is what the Brazilians enjoy today. This result is Brazil’s energy independence and cheap fuel for Brazilians. Benefits of ethanol questioned: Many experts question the benefits of ethanol in the U.S. While ethanol is being produced domestically, the plants that produce ethanol require oil as the fuel, leaving its net contribution to reducing the use of oil questionable. According to the research of David Pimental, a top agricultural expert from Cornell University, it has been calculated that powering the average U.S. automobile for one year on ethanol (blended with gasoline) derived from corn would require 11 acres of farmland, the same space needed to grow a year's supply of food for seven people. Adding up the energy costs of corn production and its conversion into ethanol, 131,000 BTUs are needed to make one gallon of ethanol. One gallon of ethanol has an energy value of only 77,000 BTUS. Thus, 70 percent more energy is required to produce ethanol than the energy that actually is in it. Every time you make one gallon of ethanol, there is a net energy loss of 54,000 BTUs”. Consequently, there is a loss of energy for ethanol as an alternative fuel source. Moreover, that does not include the trucks and the tankers involved with transport, which require oil as well. Despite the structural challenges facing ethanol, there remains a certain momentum to push this fuel as the alternative fuel to oil. Outlook:One should not be carried away with the sudden steam in the ethanol industry. The investment bankers first fueled the dotcom boom with the technology hype and then that bubble went bust. Now it appears to be the time for ethanol. What needs to be brought to an investor’s attention is that it is difficult to see how ethanol can go mainstream as a fuel if 70 percent more energy is required to produce ethanol than the energy that actually is in it. Constant recommendations to buy the stock of ethanol companies’ and all the hype that is going into ethanol appears to be temporary because the global oil prices have forced the world to seek alternative energy sources. The candidates for alternative energy like butanol, hydrogen, wind, and biomass are also under constant research and development focus. Butanol, which is produced from sugar beet, is more environmentally friendly and cheaper than ethanol. Will butanol, hydrogen, wind, and biomass be able take over ethanol’s pace? An intelligent investor will not go with the market hype and will be mindful about the threats that ethanol faces from the other sources of energy and varying crop yield controlled by the weather. At the same time it is clear ethanol is one of the options now under development within the alternative energy sector, and it needs to be monitored to determine its potential impact on efforts to expand beyond global reliance on petrochemical products. by Salman AnwarKWR International July 29th, 2006 *For more information refer to the Organization for Economic Co-operation and Development study: Bio-fuels for Transport – An international perspective (May2004) While the information and opinions contained within have been compiled from sources believed to be reliable, KWR does not represent that it is accurate or complete and it should be relied on as such. Accordingly, nothing in this article shall be construed as offering a guarantee of the accuracy or completeness of the information contained herein, or as an offer or solicitation with respect to the purchase or sale of any security. All opinions and estimates are subject to change without notice. KWR staff, consultants and contributors to the KWR International Advisor may at any time have a long or short position in any security or option mentioned. KWR International Advisor E ditor: Dr. Scott B. MacDonald, Sr. Consultant Deputy Editors: Dr. Jonathan Lemco, Director and Sr. Consultant and Robert Windorf, Senior Consultant Associate Editor: Darin Feldman Publisher: Keith W. Rabin, President Web Design: Seth Lopez, Sr. Consultant To obtain your free subscription to the KWR International Advisor, please click here to register for the KWR Advisor mailing list For information concerning advertising, please contact: Advertising@kwrintl.com Please forward all feedback, comments and submission and reproduction requests to: KWR.Advisor@kwrintl.com © 2005 KWR International, Inc. |

| Home :: Archives :: Contact |

THURSDAY EDITION July 9th, 2026 © 2026 321energy.com |

|